You might also like

- Communications Platform as a Service cPaaS A Complete GuideFrom EverandCommunications Platform as a Service cPaaS A Complete GuideNo ratings yet

- Uneecops Technologies LTDDocument12 pagesUneecops Technologies LTDRajan KumarNo ratings yet

- TCS CRM Capabilities for BFSDocument9 pagesTCS CRM Capabilities for BFSGaurav JoshiNo ratings yet

- Everest Group Price Benchmarking PrimerDocument14 pagesEverest Group Price Benchmarking PrimerCharles TuazonNo ratings yet

- Zinnov Zones For Digital Technology Services Media 160408053752Document27 pagesZinnov Zones For Digital Technology Services Media 160408053752latentpotNo ratings yet

- Gartner Market Research PrimerDocument97 pagesGartner Market Research PrimerSurya Kiran RaiNo ratings yet

- Top Faculty Tier1 EngineeringInst Sep2013Document63 pagesTop Faculty Tier1 EngineeringInst Sep2013vaibhavNo ratings yet

- SAP Business Strategy & Product Portfolio and SAP HANA Cloud OfferingDocument17 pagesSAP Business Strategy & Product Portfolio and SAP HANA Cloud OfferingVEERANo ratings yet

- About ZinnovDocument12 pagesAbout Zinnoviisc cpdmNo ratings yet

- Cloudesign Corporate ProfileDocument12 pagesCloudesign Corporate ProfileNishanth Shetty0% (1)

- Gartner Magic Quadrant For Enterprise File Synchronization and SharingDocument33 pagesGartner Magic Quadrant For Enterprise File Synchronization and SharingFirdaus Mat NayanNo ratings yet

- Multiples - JDDocument2 pagesMultiples - JDChirag KashyapNo ratings yet

- LNT Infotech Corporate Brochure PDFDocument28 pagesLNT Infotech Corporate Brochure PDFadi99123No ratings yet

- Deloitte - 2022 Global Automotive Consumer StudyDocument34 pagesDeloitte - 2022 Global Automotive Consumer StudyAakash MalhotraNo ratings yet

- Online Sales of Automotive Parts in Germany Set For Strong Growth - We Expect Online Business To Have 20% Share in 2025Document3 pagesOnline Sales of Automotive Parts in Germany Set For Strong Growth - We Expect Online Business To Have 20% Share in 2025Gsp TonyNo ratings yet

- Exalca Company Profile V 0.2Document8 pagesExalca Company Profile V 0.2Rajkumar CNo ratings yet

- AFL Corporate Overview v4.1Document29 pagesAFL Corporate Overview v4.1Sigit ArifiantoNo ratings yet

- International Expansion StrategyDocument15 pagesInternational Expansion StrategykananguptaNo ratings yet

- Everest Group - Top 20 IOT Trailblazers PDFDocument79 pagesEverest Group - Top 20 IOT Trailblazers PDFpantmukulNo ratings yet

- Resume - Rishabh WadhawanDocument2 pagesResume - Rishabh WadhawanYash WadhawanNo ratings yet

- Growth Strategy: by ICON-Consulting Club of IIM-BDocument10 pagesGrowth Strategy: by ICON-Consulting Club of IIM-BDamon SNo ratings yet

- Infosys ConsultingDocument4 pagesInfosys Consultingrush2jananiNo ratings yet

- Enterprise Service Cloud MigrationDocument10 pagesEnterprise Service Cloud MigrationAjit Kumar SubramanyamNo ratings yet

- Accenture Global Delivery Network Services OverviewDocument4 pagesAccenture Global Delivery Network Services OverviewKasim Mohammad100% (1)

- Emvigo Company ProfileDocument29 pagesEmvigo Company ProfileMasaka Cultural ResortNo ratings yet

- About Max Vision SolutionsDocument18 pagesAbout Max Vision SolutionsmaxvisionsolutionsNo ratings yet

- Felix Capability OverviewDocument12 pagesFelix Capability OverviewGagan GahlotNo ratings yet

- Wipro Project on Globalization StrategiesDocument11 pagesWipro Project on Globalization StrategiessoumyanicNo ratings yet

- 2 - New Market Entry Strategy 2019Document28 pages2 - New Market Entry Strategy 2019Sherzod AxmedovNo ratings yet

- Ajit Shukla - LinkedIn PDFDocument2 pagesAjit Shukla - LinkedIn PDFSuumit AroraNo ratings yet

- Tcs Presentation1Document14 pagesTcs Presentation1Waibhav KrishnaNo ratings yet

- Nurturing Talent - Citibank IndiaDocument1 pageNurturing Talent - Citibank IndiaPrerna MaheshwariNo ratings yet

- BOLD by DevoteamDocument6 pagesBOLD by DevoteamJoão Pedro SaraivaNo ratings yet

- HUL Finace FInalDocument9 pagesHUL Finace FInalAvijitNo ratings yet

- INDUSTRY ANALYSIS REPORT - Information Technology SECTOR Tech MahindraDocument27 pagesINDUSTRY ANALYSIS REPORT - Information Technology SECTOR Tech MahindraShutu RoyNo ratings yet

- Emerging Players in Indian Startup Funding Landscape: Micro VC Funds in IndiaDocument23 pagesEmerging Players in Indian Startup Funding Landscape: Micro VC Funds in Indiasarvagya vermaNo ratings yet

- Market Insights - Jan 2020Document5 pagesMarket Insights - Jan 2020Ankit JainNo ratings yet

- Indian Market AnalysisDocument20 pagesIndian Market AnalysisChetan SomashekarNo ratings yet

- Talent Acquisition With IBM - Precision Talent ModelDocument5 pagesTalent Acquisition With IBM - Precision Talent ModelshripadaNo ratings yet

- CV3 Surabhi Agarwal 61920586Document1 pageCV3 Surabhi Agarwal 61920586Harmandeep singhNo ratings yet

- Gartner Market Share Analysis - Security Consulting, Worldwide, 2012Document9 pagesGartner Market Share Analysis - Security Consulting, Worldwide, 2012Othon CabreraNo ratings yet

- Pricing ModelsDocument1 pagePricing ModelsJoydip MukhopadhyayNo ratings yet

- Presented By:-Anurag Nirwan, Pranjal Sharma, Diksha Srivastava, Prasad TayadeDocument21 pagesPresented By:-Anurag Nirwan, Pranjal Sharma, Diksha Srivastava, Prasad Tayadeanurag nirwan100% (1)

- Emerging Jobs Report India Sept2018-D5B5Document29 pagesEmerging Jobs Report India Sept2018-D5B5Sunny VermaNo ratings yet

- GSPR-2014 Media Version Image - FinalDocument46 pagesGSPR-2014 Media Version Image - FinalHardik TiwariNo ratings yet

- CRED Employee BrandingDocument17 pagesCRED Employee BrandingAkshayUberoiNo ratings yet

- WNS BFS Capabilities Presentation - Jan - 2013Document30 pagesWNS BFS Capabilities Presentation - Jan - 2013VikasNo ratings yet

- Sales Enablement Landscape Vol.2 2021Document66 pagesSales Enablement Landscape Vol.2 2021Bob KellyNo ratings yet

- GTM STRATEGY For Revamped Modify Journey: Freshness ReliabilityDocument16 pagesGTM STRATEGY For Revamped Modify Journey: Freshness ReliabilityAnimesh KumarNo ratings yet

- Infosys Technologies Limited: Automotive IndustryDocument19 pagesInfosys Technologies Limited: Automotive IndustrySharath ReddyNo ratings yet

- Infosys Strategy AnalysisDocument14 pagesInfosys Strategy AnalysisReshma K ChandranNo ratings yet

- E10 - Target Latin America, Middle East and Europe MarketsDocument9 pagesE10 - Target Latin America, Middle East and Europe MarketsKush234No ratings yet

- Company Profile: Uplifting Business Through TechDocument14 pagesCompany Profile: Uplifting Business Through Techammad ahmadNo ratings yet

- Commercial Lending Solution SuiteDocument4 pagesCommercial Lending Solution SuitebalegaddeNo ratings yet

- Rishabh Software: A Digital Transformation Enabler - Microsoft TechnologiesDocument24 pagesRishabh Software: A Digital Transformation Enabler - Microsoft Technologiesmasterajax44No ratings yet

- Edelweiss Tokio - IIM Lucknow - Job Description - Finals 2021Document1 pageEdelweiss Tokio - IIM Lucknow - Job Description - Finals 2021manishNo ratings yet

- openSAP Leo1 All Slides ENDocument97 pagesopenSAP Leo1 All Slides ENBryce JobsNo ratings yet

- BCG Banner7 PDFDocument23 pagesBCG Banner7 PDFAnupam LoiwalNo ratings yet

- HUL Financial ModelDocument22 pagesHUL Financial ModelMadhura SridharNo ratings yet

- Month-to-Date: Index MTD 3M YTD 12MDocument4 pagesMonth-to-Date: Index MTD 3M YTD 12MEric ReyesNo ratings yet

- 3 H OmDocument13 pages3 H OmRohit Zende.No ratings yet

- CLTLDocument8 pagesCLTLVijay RamanNo ratings yet

- AD-times Wipro 2018Document12 pagesAD-times Wipro 2018Vijay RamanNo ratings yet

- CLTLDocument8 pagesCLTLVijay RamanNo ratings yet

- d.light's Channel Strategy Challenges in Rural IndiaDocument3 pagesd.light's Channel Strategy Challenges in Rural IndiaHans BerlinNo ratings yet

- CollectableToysasMarketingTools UnderstandingPreschoolChildrensResponsesJPPM2012Document13 pagesCollectableToysasMarketingTools UnderstandingPreschoolChildrensResponsesJPPM2012Vijay RamanNo ratings yet

- SalesDocument11 pagesSalesVijay RamanNo ratings yet

- Operations Dossier + FAQ's 2018-19 PDFDocument93 pagesOperations Dossier + FAQ's 2018-19 PDFVijay RamanNo ratings yet

- Si HCLDocument8 pagesSi HCLVijay RamanNo ratings yet

- Frozen Food MarketDocument13 pagesFrozen Food MarketVijay RamanNo ratings yet

- Researching MarketsDocument4 pagesResearching MarketsVijay RamanNo ratings yet

- EMEDocument74 pagesEMEVijay RamanNo ratings yet

- Industry Presentation: Group 25Document18 pagesIndustry Presentation: Group 25Vijay RamanNo ratings yet

- CarWale Product Manager RoleDocument2 pagesCarWale Product Manager RoleVijay RamanNo ratings yet

- B2B Sealed Air Q1Document1 pageB2B Sealed Air Q1Vijay RamanNo ratings yet

- 3 H OmDocument13 pages3 H OmRohit Zende.No ratings yet

- Adtimes ABFRL 2018Document10 pagesAdtimes ABFRL 2018Vijay RamanNo ratings yet

- Liberalisation and Impact On Various SectorsDocument13 pagesLiberalisation and Impact On Various SectorsVijay RamanNo ratings yet

- Threat of New Entrants in Banking Industry Due to High Entry BarriersDocument4 pagesThreat of New Entrants in Banking Industry Due to High Entry BarriersVijay RamanNo ratings yet

- AD-Times Asian Paints 2018Document15 pagesAD-Times Asian Paints 2018Vijay RamanNo ratings yet

- ADTimes Cummins 2018Document26 pagesADTimes Cummins 2018Vijay RamanNo ratings yet

- Sector Study AviationDocument12 pagesSector Study AviationVijay RamanNo ratings yet

- Air India2Document4 pagesAir India2Vijay RamanNo ratings yet

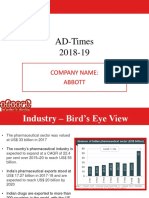

- ADtimes Abbott 2018Document9 pagesADtimes Abbott 2018Vijay RamanNo ratings yet

- Pre-Sales EngineerDocument2 pagesPre-Sales Engineerapi-79295866No ratings yet

- BCK ChalisaDocument43 pagesBCK ChalisasuyashNo ratings yet

- 3-IBM-RB - Sales - Selling Ibm Innovative SolutionsDocument226 pages3-IBM-RB - Sales - Selling Ibm Innovative Solutionsjusak131No ratings yet

- What is turn-around strategy & IBM's exampleDocument11 pagesWhat is turn-around strategy & IBM's exampleNagen Kakati100% (1)

- IBM Cloud Computing Case StudiesDocument14 pagesIBM Cloud Computing Case StudiesLilchunky100% (1)

- IBM White Paper-Value of TrainingDocument14 pagesIBM White Paper-Value of TrainingPriyanka BachhanNo ratings yet

- Lucy ChanDocument16 pagesLucy ChanGopiKrishnan PlakkatNo ratings yet

- BEC Practice 4Document6 pagesBEC Practice 4Trần ThơmNo ratings yet

- Case Study Analysis 1 3Document5 pagesCase Study Analysis 1 3John Raven Tobeo100% (1)

- Myer Website Crash Due to IBM Communication BreakdownDocument2 pagesMyer Website Crash Due to IBM Communication Breakdownvishal_debnathNo ratings yet

- Oracle On IBM Power - Level 1 QuizDocument14 pagesOracle On IBM Power - Level 1 QuizNatnael Kora100% (1)

- Finance Director in Denver CO Resume Victoria NaugleDocument2 pagesFinance Director in Denver CO Resume Victoria NaugleVictoriaNaugleNo ratings yet

- 1 - Management and OrganizationDocument22 pages1 - Management and OrganizationDang Nguyen0% (1)

- Starbucks B2B PlanDocument52 pagesStarbucks B2B Planbobbyend0% (1)

- Migration Services IBM Tivoli Workload AutomationDocument7 pagesMigration Services IBM Tivoli Workload AutomationautomaticitNo ratings yet

- IBM Red Bank Smarter BankingDocument210 pagesIBM Red Bank Smarter BankingWong Wong WLNo ratings yet

- Leveraging DB2 10 For High Performance of Your Data Warehouse PDFDocument218 pagesLeveraging DB2 10 For High Performance of Your Data Warehouse PDFRrguyyalaNo ratings yet

- Senior IT Project Manager in Austin TX TN Resume Charley GrayDocument6 pagesSenior IT Project Manager in Austin TX TN Resume Charley GrayCharleyGrayNo ratings yet

- Talent and Workforce ManagementDocument8 pagesTalent and Workforce ManagementyessirNo ratings yet

- IBM MMS For Cisco FLYER-IBMTSS-MMSFORCISCO PDFDocument2 pagesIBM MMS For Cisco FLYER-IBMTSS-MMSFORCISCO PDFMaarten FolmerNo ratings yet

- Cathay PacificDocument6 pagesCathay PacificIIMnotes100% (1)

- IBM Graduate Application FormDocument2 pagesIBM Graduate Application FormNikos Papageorgiou50% (2)

- IBM Connections 5 BrochureDocument6 pagesIBM Connections 5 BrochureTaqwa ManNo ratings yet

- Search Suggestions: Popular Searches: Cost Accounting CoursesDocument21 pagesSearch Suggestions: Popular Searches: Cost Accounting CoursesYassi CurtisNo ratings yet

- TXSeries For Multiplatforms Using IBM Communications Server For AIX With CICS Version 6.2Document75 pagesTXSeries For Multiplatforms Using IBM Communications Server For AIX With CICS Version 6.2deisecairoNo ratings yet

- IBM India JobsDocument1 pageIBM India JobsArun SinghNo ratings yet

- Application Modernization On IBM PowerDocument17 pagesApplication Modernization On IBM Powertianmo1994No ratings yet

- Ibm WikiDocument6 pagesIbm WikissmeeshiNo ratings yet

- Five Ways Artificial Intelligence and Machine Learning Deliver Business Impacts - GartnerDocument8 pagesFive Ways Artificial Intelligence and Machine Learning Deliver Business Impacts - GartnerKeren MendesNo ratings yet

- Storage For Z L1 Seller PresentationDocument69 pagesStorage For Z L1 Seller PresentationElisa GarciaRNo ratings yet

- Digital Gold: Bitcoin and the Inside Story of the Misfits and Millionaires Trying to Reinvent MoneyFrom EverandDigital Gold: Bitcoin and the Inside Story of the Misfits and Millionaires Trying to Reinvent MoneyRating: 4 out of 5 stars4/5 (51)

- ChatGPT Side Hustles 2024 - Unlock the Digital Goldmine and Get AI Working for You Fast with More Than 85 Side Hustle Ideas to Boost Passive Income, Create New Cash Flow, and Get Ahead of the CurveFrom EverandChatGPT Side Hustles 2024 - Unlock the Digital Goldmine and Get AI Working for You Fast with More Than 85 Side Hustle Ideas to Boost Passive Income, Create New Cash Flow, and Get Ahead of the CurveNo ratings yet

- Defensive Cyber Mastery: Expert Strategies for Unbeatable Personal and Business SecurityFrom EverandDefensive Cyber Mastery: Expert Strategies for Unbeatable Personal and Business SecurityRating: 5 out of 5 stars5/5 (1)

- Cyber War: The Next Threat to National Security and What to Do About ItFrom EverandCyber War: The Next Threat to National Security and What to Do About ItRating: 3.5 out of 5 stars3.5/5 (66)

- Scary Smart: The Future of Artificial Intelligence and How You Can Save Our WorldFrom EverandScary Smart: The Future of Artificial Intelligence and How You Can Save Our WorldRating: 4.5 out of 5 stars4.5/5 (54)

- CompTIA Security+ Get Certified Get Ahead: SY0-701 Study GuideFrom EverandCompTIA Security+ Get Certified Get Ahead: SY0-701 Study GuideRating: 5 out of 5 stars5/5 (2)

- Algorithms to Live By: The Computer Science of Human DecisionsFrom EverandAlgorithms to Live By: The Computer Science of Human DecisionsRating: 4.5 out of 5 stars4.5/5 (722)

- Chaos Monkeys: Obscene Fortune and Random Failure in Silicon ValleyFrom EverandChaos Monkeys: Obscene Fortune and Random Failure in Silicon ValleyRating: 3.5 out of 5 stars3.5/5 (111)

- The Infinite Machine: How an Army of Crypto-Hackers Is Building the Next Internet with EthereumFrom EverandThe Infinite Machine: How an Army of Crypto-Hackers Is Building the Next Internet with EthereumRating: 3 out of 5 stars3/5 (12)

- ChatGPT Millionaire 2024 - Bot-Driven Side Hustles, Prompt Engineering Shortcut Secrets, and Automated Income Streams that Print Money While You Sleep. The Ultimate Beginner’s Guide for AI BusinessFrom EverandChatGPT Millionaire 2024 - Bot-Driven Side Hustles, Prompt Engineering Shortcut Secrets, and Automated Income Streams that Print Money While You Sleep. The Ultimate Beginner’s Guide for AI BusinessNo ratings yet

- The Intel Trinity: How Robert Noyce, Gordon Moore, and Andy Grove Built the World's Most Important CompanyFrom EverandThe Intel Trinity: How Robert Noyce, Gordon Moore, and Andy Grove Built the World's Most Important CompanyNo ratings yet

- Chip War: The Quest to Dominate the World's Most Critical TechnologyFrom EverandChip War: The Quest to Dominate the World's Most Critical TechnologyRating: 4.5 out of 5 stars4.5/5 (227)

- The Corporate Startup: How established companies can develop successful innovation ecosystemsFrom EverandThe Corporate Startup: How established companies can develop successful innovation ecosystemsRating: 4 out of 5 stars4/5 (6)

- Generative AI: The Insights You Need from Harvard Business ReviewFrom EverandGenerative AI: The Insights You Need from Harvard Business ReviewRating: 4.5 out of 5 stars4.5/5 (2)

- The Future of Geography: How the Competition in Space Will Change Our WorldFrom EverandThe Future of Geography: How the Competition in Space Will Change Our WorldRating: 4.5 out of 5 stars4.5/5 (4)

- Artificial Intelligence: A Guide for Thinking HumansFrom EverandArtificial Intelligence: A Guide for Thinking HumansRating: 4.5 out of 5 stars4.5/5 (30)

- Reality+: Virtual Worlds and the Problems of PhilosophyFrom EverandReality+: Virtual Worlds and the Problems of PhilosophyRating: 4 out of 5 stars4/5 (24)

- The Master Algorithm: How the Quest for the Ultimate Learning Machine Will Remake Our WorldFrom EverandThe Master Algorithm: How the Quest for the Ultimate Learning Machine Will Remake Our WorldRating: 4.5 out of 5 stars4.5/5 (107)

- Pick Three: You Can Have It All (Just Not Every Day)From EverandPick Three: You Can Have It All (Just Not Every Day)Rating: 4.5 out of 5 stars4.5/5 (4)

- AI Superpowers: China, Silicon Valley, and the New World OrderFrom EverandAI Superpowers: China, Silicon Valley, and the New World OrderRating: 4.5 out of 5 stars4.5/5 (398)

- Everybody Lies: Big Data, New Data, and What the Internet Can Tell Us About Who We Really AreFrom EverandEverybody Lies: Big Data, New Data, and What the Internet Can Tell Us About Who We Really AreRating: 4.5 out of 5 stars4.5/5 (911)