You might also like

- Accounting Principles Chapter 7 Solution ManualDocument123 pagesAccounting Principles Chapter 7 Solution ManualKitchen UselessNo ratings yet

- Instructors: Beppino PasqualiDocument10 pagesInstructors: Beppino PasqualiAayush AgarwalNo ratings yet

- Financial Accounting: Theory and Analysis: Text and Cases 13 EditionDocument56 pagesFinancial Accounting: Theory and Analysis: Text and Cases 13 EditionLIZNo ratings yet

- INTERNSHIP REPORT On LatherDocument52 pagesINTERNSHIP REPORT On LatherSub 1No ratings yet

- Philippines Court Case Affidavit Estafa InvestmentDocument6 pagesPhilippines Court Case Affidavit Estafa InvestmentRhic Ryanlhee Vergara Fabs100% (6)

- BASIX Thermal Comfort Protocols Mar09Document23 pagesBASIX Thermal Comfort Protocols Mar09Ray LeungNo ratings yet

- GRI2009 EBrochureDocument27 pagesGRI2009 EBrochurenjaloualiNo ratings yet

- Method Statement For Painting System KAFD-RY-RIA2-CP04-SAB-ARF-MES-05001 Rev.01Document13 pagesMethod Statement For Painting System KAFD-RY-RIA2-CP04-SAB-ARF-MES-05001 Rev.01khalid khanNo ratings yet

- Customer-Partners - WINDOW-POC GUIDE Harmony EndPoint EPM R81.10 - Step by Step Version FinalDocument39 pagesCustomer-Partners - WINDOW-POC GUIDE Harmony EndPoint EPM R81.10 - Step by Step Version Finalgarytj210% (1)

- MBBcurrent 564548147990 2022-09-30 PDFDocument12 pagesMBBcurrent 564548147990 2022-09-30 PDFAdeela fazlinNo ratings yet

- Talent management roadmap for SMB growth and expansionDocument10 pagesTalent management roadmap for SMB growth and expansionElio ZerpaNo ratings yet

- SDS-Tulip Spray (EN)Document12 pagesSDS-Tulip Spray (EN)Ratna SpotifyNo ratings yet

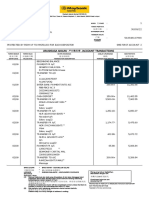

- Statement PDFDocument7 pagesStatement PDFGovardhanGurramNo ratings yet

- Robin Lohre vs. Posh Maids, Et. Al.Document6 pagesRobin Lohre vs. Posh Maids, Et. Al.NickNo ratings yet

- Entrepreneurship Notes - Da II-1-2Document520 pagesEntrepreneurship Notes - Da II-1-2mzee wasaundiNo ratings yet

- Audit Committee Characteristics and Tax Aggressiveness: Manon Deslandes Anne Fortin Suzanne LandryDocument22 pagesAudit Committee Characteristics and Tax Aggressiveness: Manon Deslandes Anne Fortin Suzanne LandryAnin YusufNo ratings yet

- Study of Quality Testing of Milk Powder in SterlinDocument3 pagesStudy of Quality Testing of Milk Powder in SterlinMuratNo ratings yet

- F8 AOF Question Book - Jan 2021Document47 pagesF8 AOF Question Book - Jan 2021Linh NguyenNo ratings yet

- ARA Compendium - Oct 2017 - Edelweiss PDFDocument188 pagesARA Compendium - Oct 2017 - Edelweiss PDFAnish TeliNo ratings yet

- 20200912024944SLCHIA005MA2 Slides CostsDocument104 pages20200912024944SLCHIA005MA2 Slides CostsDương DươngNo ratings yet

- Curso HitachiDocument3 pagesCurso HitachiJoão De Deus Oliveira CriscuoloNo ratings yet

- ArulAshish (10y 0m)Document2 pagesArulAshish (10y 0m)Lingesh SNo ratings yet

- Navitasys India Private Limited: Project: VECTORDocument14 pagesNavitasys India Private Limited: Project: VECTORSagar Garg (IN)No ratings yet

- 10 1108 - Ajar 11 2020 0121Document22 pages10 1108 - Ajar 11 2020 0121Dina NellysaNo ratings yet

- SGS MIN TP2003 10 Coal Quality Management PDFDocument4 pagesSGS MIN TP2003 10 Coal Quality Management PDFDavid SimanungkalitNo ratings yet

- Emsu0138Document2 pagesEmsu0138Mohanned KhalidNo ratings yet

- Say It With Charts - McKinsey-28Document4 pagesSay It With Charts - McKinsey-28YONGXING CHENNo ratings yet

- FHS 2016-19 CIP July 9 2017 - WebsiteDocument23 pagesFHS 2016-19 CIP July 9 2017 - Website愛.NiniNo ratings yet

- Bell KJ Thesis 1Document308 pagesBell KJ Thesis 1Aisyah RahmawatiNo ratings yet

- Cakpo T. Paul Luc U: Who I'Am Personal InformationDocument4 pagesCakpo T. Paul Luc U: Who I'Am Personal Informationchancia angeNo ratings yet

- Zemen Bank Annual Report 2010Document21 pagesZemen Bank Annual Report 2010Habtamu R.No ratings yet

- QF-MKT-06 Cust - SpecificDocument19 pagesQF-MKT-06 Cust - SpecificVirendra KumarNo ratings yet

- Q1 2021 Earnings Call: Strategic Priorities and Financial ResultsDocument35 pagesQ1 2021 Earnings Call: Strategic Priorities and Financial ResultsMohit SinghNo ratings yet

- Financial Statement Analysis and Security Valuation: - October 26, 2022 Arnt VerriestDocument42 pagesFinancial Statement Analysis and Security Valuation: - October 26, 2022 Arnt VerriestfelipeNo ratings yet

- Academy Module 1 Slides DOWNLOADDocument31 pagesAcademy Module 1 Slides DOWNLOADmissdvNo ratings yet

- RJR v. Bonta - Emergency Application For Writ of InjunctionDocument55 pagesRJR v. Bonta - Emergency Application For Writ of Injunctioncharlie minatoNo ratings yet

- Receiving process overviewDocument19 pagesReceiving process overviewRx DentviewNo ratings yet

- Strategy Data Reading ReferenceDocument2 pagesStrategy Data Reading ReferenceyyyNo ratings yet

- Avalon Power Pvt. Ltd. PSA Oxygen Generation Solutions ManufacturerDocument26 pagesAvalon Power Pvt. Ltd. PSA Oxygen Generation Solutions ManufacturerPraveenNo ratings yet

- Max Badi Waali PDFDocument171 pagesMax Badi Waali PDFarshad khanNo ratings yet

- Pr6 Gp6Document46 pagesPr6 Gp6Kwang Yi JuinNo ratings yet

- 1.1 Overview STCWDocument39 pages1.1 Overview STCWmonica matualageNo ratings yet

- Research - Azeem!Document18 pagesResearch - Azeem!Niyati ShuklaNo ratings yet

- AJCR - Vol.4 - Special Issue - 2011Document190 pagesAJCR - Vol.4 - Special Issue - 2011NURUL AMALINA BINTI ROSLI STUDENTNo ratings yet

- ExP Class NotesDocument38 pagesExP Class NotesEltonNo ratings yet

- Deloitte Belgium - Working Capital in Industrial ProductsDocument12 pagesDeloitte Belgium - Working Capital in Industrial ProductsNayoung LeeNo ratings yet

- Corporate Reporting and GovernanceDocument210 pagesCorporate Reporting and Governanceisabella ayikuNo ratings yet

- bms.0930 r0 Management Reviews PDFDocument2 pagesbms.0930 r0 Management Reviews PDFYahia Mustafa AlfazaziNo ratings yet

- Manual MPDocument162 pagesManual MPRoberto VictoriaNo ratings yet

- Course Info MGT787Document11 pagesCourse Info MGT787MAISARANo ratings yet

- Corporate Governance and Its Efficacy in The Present EraDocument17 pagesCorporate Governance and Its Efficacy in The Present EraNandini ChandraNo ratings yet

- Hse Accountability FrameworkDocument8 pagesHse Accountability FrameworkNisith SahooNo ratings yet

- FR17 - Employee Benefits (Stud) .Document45 pagesFR17 - Employee Benefits (Stud) .duong duongNo ratings yet

- KASHIF KAMRAN ACCA NOTES Combined Block A NotesDocument46 pagesKASHIF KAMRAN ACCA NOTES Combined Block A NotesGeoNo ratings yet

- Bajaj Finance - MOA and AOADocument77 pagesBajaj Finance - MOA and AOAPrathikNo ratings yet

- Bos 51127Document274 pagesBos 51127bhagirath prakrutNo ratings yet

- Inventory Report of Assets and Liabilities Capital BankDocument50 pagesInventory Report of Assets and Liabilities Capital BankFuaad DodooNo ratings yet

- The Effectiveness of Communication in Software Development Project ManagementDocument10 pagesThe Effectiveness of Communication in Software Development Project ManagementeduardompferreiraNo ratings yet

- 7 Investment PolicyDocument87 pages7 Investment PolicyShaurya Singh100% (1)

- Cloud Economics and Billing Module 2Document60 pagesCloud Economics and Billing Module 2Madhuka DilshanNo ratings yet

- Resume FinalDocument2 pagesResume Finalapi-617160854No ratings yet

- Attachment Example of Lone Working Risk AssessmentDocument8 pagesAttachment Example of Lone Working Risk AssessmentRodrigoNo ratings yet

- Materials Setup in FCS V6 (ENHANCED Version) PDFDocument44 pagesMaterials Setup in FCS V6 (ENHANCED Version) PDFRx DentviewNo ratings yet

- Financial Accounting: Theory and Analysis: Text and Cases 12 EditionDocument43 pagesFinancial Accounting: Theory and Analysis: Text and Cases 12 EditionmohammadNo ratings yet

- Minggu 2Document64 pagesMinggu 2Tanya RexanneNo ratings yet

- Sensation and PerceptionDocument219 pagesSensation and PerceptionLIZNo ratings yet

- Notes - Neural DevelopmentDocument5 pagesNotes - Neural DevelopmentLIZNo ratings yet

- Neurotransmitters NotesDocument5 pagesNeurotransmitters NotesLIZNo ratings yet

- Bayesian Lecture NotesDocument28 pagesBayesian Lecture NotesLIZNo ratings yet

- ActionPotentials NotesDocument7 pagesActionPotentials NotesLIZNo ratings yet

- Summary Sleepdepri SetDocument5 pagesSummary Sleepdepri SetLIZNo ratings yet

- Ief Exercises Chptrs 14 15Document13 pagesIef Exercises Chptrs 14 15LIZNo ratings yet

- Peer Review Wave 4 InstructionsDocument1 pagePeer Review Wave 4 InstructionsLIZNo ratings yet

- Liz Gene SummariesDocument7 pagesLiz Gene SummariesLIZNo ratings yet

- OSHMM DA 01 - Maintenance of Safety and Operational EquipmentDocument2 pagesOSHMM DA 01 - Maintenance of Safety and Operational EquipmentIoannis FinaruNo ratings yet

- Faith Leaders Letter Ohio SB3Document4 pagesFaith Leaders Letter Ohio SB3WKYC.comNo ratings yet

- Career in criminal law and role of a criminal lawyerDocument6 pagesCareer in criminal law and role of a criminal lawyerAnkush JadaunNo ratings yet

- FULL TEXT - Go vs. CADocument26 pagesFULL TEXT - Go vs. CASSNo ratings yet

- Norma Astm A 148pdfDocument3 pagesNorma Astm A 148pdfLeo AislanNo ratings yet

- Lauren J. Paulson, Magnum Opus, FAITHLESS IN FORECLOSURE, How 14 Fourteen Judges Took My HomeDocument55 pagesLauren J. Paulson, Magnum Opus, FAITHLESS IN FORECLOSURE, How 14 Fourteen Judges Took My HomeBiloxiMarx100% (1)

- NAKIVO Price ListDocument1 pageNAKIVO Price ListBiju ThankappanNo ratings yet

- Electric Field IntensityDocument11 pagesElectric Field IntensityRussia ServerNo ratings yet

- The Environmental Impact Assessment in Sri Lanka: Deshan BandaraDocument65 pagesThe Environmental Impact Assessment in Sri Lanka: Deshan BandaraVindula RanawakaNo ratings yet

- Islamic Political PhilosophyDocument8 pagesIslamic Political PhilosophyKhalil-Ur RehmanNo ratings yet

- Smart Home 9504 PDFDocument28 pagesSmart Home 9504 PDFJefferson ClaytonNo ratings yet

- Goeller, M. - The Bishop - S Opening PDFDocument39 pagesGoeller, M. - The Bishop - S Opening PDFleonilsonsvNo ratings yet

- How To Qualify For A Cpa LicenseDocument2 pagesHow To Qualify For A Cpa LicenseRushabh ChitaliaNo ratings yet

- Management ProjectDocument20 pagesManagement ProjectPrasad BhumkarNo ratings yet

- Finals Quiz #2 Soce, Soci, Ahfs and Do Multiple Choice: Account Title AmountDocument3 pagesFinals Quiz #2 Soce, Soci, Ahfs and Do Multiple Choice: Account Title AmountNew TonNo ratings yet

- Bank account transactions and financial recordsDocument5 pagesBank account transactions and financial recordsSyaza AisyahNo ratings yet

- UPSC Public Administration Syllabus for IAS Mains ExamDocument6 pagesUPSC Public Administration Syllabus for IAS Mains ExamluvNo ratings yet

- National Bravery Awards - Sub GK 1 To 4Document4 pagesNational Bravery Awards - Sub GK 1 To 4lafdebazNo ratings yet

- Oblicon PremidDocument30 pagesOblicon PremidArwella Gregorio100% (1)

- Pedro Pelaez PDFDocument22 pagesPedro Pelaez PDFAdrian Garett SianNo ratings yet

- Bus Driver CV TemplateDocument2 pagesBus Driver CV Templatecucucucucu72No ratings yet

- Saramati FormDocument4 pagesSaramati FormSivadasankk KolurkavilNo ratings yet

- Perpetual Inventory SystemDocument6 pagesPerpetual Inventory SystemJonalyn DicdicanNo ratings yet

- Clara Schwartz: A Deadly Game: Perdum Mihai Drept Anul II ZIDocument14 pagesClara Schwartz: A Deadly Game: Perdum Mihai Drept Anul II ZIMihai PerdumNo ratings yet

- Nathaniel Hawthorne's The Shaker Bridal StoryDocument11 pagesNathaniel Hawthorne's The Shaker Bridal StoryGabriel Severo Marques100% (2)

- Constitutional Law Online Class - 06: Fundamental Rights & Their Enforcement - Human RightsDocument14 pagesConstitutional Law Online Class - 06: Fundamental Rights & Their Enforcement - Human RightsRAGIB SHAHRIAR RAFINo ratings yet