You might also like

- Introduction to Negotiable Instruments: As per Indian LawsFrom EverandIntroduction to Negotiable Instruments: As per Indian LawsRating: 5 out of 5 stars5/5 (1)

- Fundamentals of Business Law PDFDocument358 pagesFundamentals of Business Law PDFmikiyo90% (10)

- Check Vs DraftDocument15 pagesCheck Vs DraftJoshua Capa FrondaNo ratings yet

- Bill of Exchange PDFDocument52 pagesBill of Exchange PDFParesh Vaviya91% (11)

- Export Credit Guarantee Corporation of India (ECGC)Document20 pagesExport Credit Guarantee Corporation of India (ECGC)devaNo ratings yet

- DDFDocument66 pagesDDFPankaj Kumar100% (2)

- Harshad Mehta Scam: Made By: Akshay VirkarDocument17 pagesHarshad Mehta Scam: Made By: Akshay Virkarseema sweetNo ratings yet

- Harshad Mehta CaseDocument16 pagesHarshad Mehta Casegunjan67% (3)

- Special Commercial Laws Midterm NotesDocument47 pagesSpecial Commercial Laws Midterm NotesVirneeJoyNo ratings yet

- Letter of CreditDocument5 pagesLetter of CreditnavreenNo ratings yet

- Module 1 For Acctg 3119 - Auditing and Assurance PrinciplesDocument21 pagesModule 1 For Acctg 3119 - Auditing and Assurance PrinciplesJamille Causing AgsamosamNo ratings yet

- Harshad Mehta ScamDocument9 pagesHarshad Mehta ScamMashboob R.MNo ratings yet

- Letter of Credit and Its TypesDocument3 pagesLetter of Credit and Its TypesckapasiNo ratings yet

- ISO-TS 16949 Practice TestDocument18 pagesISO-TS 16949 Practice TestManan Bakshi100% (1)

- Fact Sheet - ITIL® 4 Specialist - Create, Deliver and Support - ClassroomDocument6 pagesFact Sheet - ITIL® 4 Specialist - Create, Deliver and Support - ClassroomEduardo MucajiNo ratings yet

- Assignment On Harshad Mehta Scam BY Parth LaddaDocument9 pagesAssignment On Harshad Mehta Scam BY Parth LaddaParth LaddaNo ratings yet

- Role of Artificial Intelligence in Banking SectorDocument45 pagesRole of Artificial Intelligence in Banking Sectorsamyak gangwal86% (7)

- 5.tender Process N DocumentationDocument35 pages5.tender Process N DocumentationDilanka MJ Dassanayake100% (1)

- Commercial Law Reviewer, MercantileDocument60 pagesCommercial Law Reviewer, MercantilecelestezerosevenNo ratings yet

- Harshad Mehta ScamDocument17 pagesHarshad Mehta ScamJaywanti Akshra GurbaniNo ratings yet

- Harshad Mehta ScamDocument16 pagesHarshad Mehta ScamArchit JainNo ratings yet

- Harshad MehtaDocument10 pagesHarshad MehtaKrutika AbitkarNo ratings yet

- Nitin - Harshad Mehta Scam PDFDocument12 pagesNitin - Harshad Mehta Scam PDFAnkit SangwanNo ratings yet

- 15 - Chapter 6 PDFDocument33 pages15 - Chapter 6 PDFTejasNo ratings yet

- Harshad Mehta ScamDocument12 pagesHarshad Mehta Scamsudhir100% (1)

- Harsad 1Document2 pagesHarsad 1Anish DhakalNo ratings yet

- Harshad Mehta ScamDocument5 pagesHarshad Mehta ScamKriti ShahNo ratings yet

- 1992 Stock Exchange ScamDocument17 pages1992 Stock Exchange Scamsidd2206No ratings yet

- Harshad Mehta Stock Market Scam 1992Document10 pagesHarshad Mehta Stock Market Scam 1992Darshan PatelNo ratings yet

- Harshad Mehta ScamDocument6 pagesHarshad Mehta ScamPraful SharmaNo ratings yet

- Harshad Mehta: What All He DidDocument4 pagesHarshad Mehta: What All He DidPrakashramkumharNo ratings yet

- Harshad Shantilal MehtaDocument10 pagesHarshad Shantilal MehtaRishi JainNo ratings yet

- Harshat Mehta's ScamDocument7 pagesHarshat Mehta's Scamseeta guptaNo ratings yet

- Harshad MehtaDocument6 pagesHarshad MehtaBenika RajputNo ratings yet

- Harshad Mehta ScamDocument28 pagesHarshad Mehta Scamjoseph_kachappilly0% (1)

- Booms & Busts in Indian Share MarketDocument55 pagesBooms & Busts in Indian Share MarketAnkur GargNo ratings yet

- Teaching Note On Financial StatementsDocument28 pagesTeaching Note On Financial StatementsAvirup ChakrabortyNo ratings yet

- Anatomy of Securities Scam, 1992Document6 pagesAnatomy of Securities Scam, 1992sandipkodgire1No ratings yet

- Harshad MehtaDocument3 pagesHarshad MehtaThakurNo ratings yet

- Harshad Shantilal MehtaDocument3 pagesHarshad Shantilal MehtaSharvil GupteNo ratings yet

- The 1992 Scam: Brokerage FirmsDocument4 pagesThe 1992 Scam: Brokerage FirmsNishad JoshiNo ratings yet

- Financial Markets and Services: Ishika Manisha JyotiDocument17 pagesFinancial Markets and Services: Ishika Manisha JyotiIshika GargNo ratings yet

- Int Trade PaymentsDocument32 pagesInt Trade PaymentsRoland LeongNo ratings yet

- Keac 108Document52 pagesKeac 108DrRiitesh SinhaNo ratings yet

- Art48 SsDocument4 pagesArt48 SsmeetwithsanjayNo ratings yet

- Part 1. Letters of CreditDocument7 pagesPart 1. Letters of CreditApostol GuiaNo ratings yet

- Compiled Digests Letters of CreditDocument9 pagesCompiled Digests Letters of CreditAnonymous XvwKtnSrMRNo ratings yet

- What Happened in 1992Document22 pagesWhat Happened in 1992rahul19novNo ratings yet

- Keac 108Document52 pagesKeac 108Ias Aspirant AbhiNo ratings yet

- BNKINGDocument6 pagesBNKINGjyotiprashad041No ratings yet

- Banking Law 100marks March April 2023 (Dec 2022)Document7 pagesBanking Law 100marks March April 2023 (Dec 2022)Veena T NNo ratings yet

- 28902cpt Fa SM Cp7 Part3Document49 pages28902cpt Fa SM Cp7 Part3BasappaSarkarNo ratings yet

- Harshad Mehta: "The Big Bull" Gone WildDocument28 pagesHarshad Mehta: "The Big Bull" Gone WildShubhamNo ratings yet

- Harshad M Mehta (Document2 pagesHarshad M Mehta (Joseph JenningsNo ratings yet

- Basic Banking TermsDocument5 pagesBasic Banking Termsjain_lalita89No ratings yet

- Lecture Murahaba Bba8Document35 pagesLecture Murahaba Bba8UmairSadiq100% (1)

- #02 - Service Products of BanksDocument9 pages#02 - Service Products of BanksiitbhuNo ratings yet

- Harshad MehtaDocument3 pagesHarshad MehtaPratick GaraiNo ratings yet

- Securities Fraud in IndiaDocument14 pagesSecurities Fraud in IndiaMukundMultani100% (1)

- Money - Credit Class 10Document1 pageMoney - Credit Class 10Legendary Pokemon Blaster 2406No ratings yet

- 2DC-LC Intro PDFDocument4 pages2DC-LC Intro PDFM Ali FiazNo ratings yet

- ScamDocument21 pagesScamK SATHVIK HU21MGMT0100321No ratings yet

- History of Financial ScamsDocument18 pagesHistory of Financial ScamsLilith Karri'sNo ratings yet

- Insider's Keys: To The Best Rates And Terms On Your Next Mortgage, #1From EverandInsider's Keys: To The Best Rates And Terms On Your Next Mortgage, #1No ratings yet

- Case 007Document5 pagesCase 007Anish DhakalNo ratings yet

- Case 0004Document3 pagesCase 0004Anish DhakalNo ratings yet

- Case 0006Document2 pagesCase 0006Anish DhakalNo ratings yet

- Case 008Document6 pagesCase 008Anish DhakalNo ratings yet

- Case 0001Document3 pagesCase 0001Anish DhakalNo ratings yet

- Case 0002Document3 pagesCase 0002Anish DhakalNo ratings yet

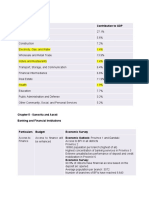

- Chapter 12: Social Sector: 1. EducationDocument3 pagesChapter 12: Social Sector: 1. EducationAnish DhakalNo ratings yet

- Case 0009Document2 pagesCase 0009Anish DhakalNo ratings yet

- Case 0007Document2 pagesCase 0007Anish DhakalNo ratings yet

- Case 0003Document3 pagesCase 0003Anish DhakalNo ratings yet

- Case 0010Document2 pagesCase 0010Anish DhakalNo ratings yet

- Browser WarsDocument2 pagesBrowser WarsAnish DhakalNo ratings yet

- Slide Change: Chapter 9 - Industry, Commerce, Supplies, and Tourism IndustryDocument3 pagesSlide Change: Chapter 9 - Industry, Commerce, Supplies, and Tourism IndustryAnish DhakalNo ratings yet

- Anish Dhakal: 19308 1992: Harshad Mehta Stock Market Scam: Big Bull of Indian Stock MarketDocument3 pagesAnish Dhakal: 19308 1992: Harshad Mehta Stock Market Scam: Big Bull of Indian Stock MarketAnish DhakalNo ratings yet

- Harsad 1Document2 pagesHarsad 1Anish DhakalNo ratings yet

- 4.3 Operational Definition of Elements of Conceptual FrameworkDocument2 pages4.3 Operational Definition of Elements of Conceptual FrameworkAnish DhakalNo ratings yet

- Case 000000002Document3 pagesCase 000000002Anish DhakalNo ratings yet

- Harsad 4Document2 pagesHarsad 4Anish DhakalNo ratings yet

- Case 000000001Document3 pagesCase 000000001Anish DhakalNo ratings yet

- Harsad 3Document3 pagesHarsad 3Anish DhakalNo ratings yet

- Harsad 2Document2 pagesHarsad 2Anish DhakalNo ratings yet

- M 4Document2 pagesM 4Anish DhakalNo ratings yet

- Background of The Study 1.1. BackgroundDocument2 pagesBackground of The Study 1.1. BackgroundAnish DhakalNo ratings yet

- 4.4 Further Findings of The StudyDocument3 pages4.4 Further Findings of The StudyAnish DhakalNo ratings yet

- M 5Document2 pagesM 5Anish DhakalNo ratings yet

- Monthly Income (In NRS) : Table 4: Frequency of Monthly Income of The RespondentsDocument3 pagesMonthly Income (In NRS) : Table 4: Frequency of Monthly Income of The RespondentsAnish DhakalNo ratings yet

- 4.4.4 Impulse Buying Behavior and Purchase Intention From MinisoDocument2 pages4.4.4 Impulse Buying Behavior and Purchase Intention From MinisoAnish DhakalNo ratings yet

- M 6Document3 pagesM 6Anish DhakalNo ratings yet

- Review of Literature 2.1. Literature ReviewDocument2 pagesReview of Literature 2.1. Literature ReviewAnish DhakalNo ratings yet

- The Rise of NFT FundraisingDocument36 pagesThe Rise of NFT FundraisingTrader CatNo ratings yet

- Major Project - AmolDocument47 pagesMajor Project - AmolAmol ShikariNo ratings yet

- Great To Have You On Board!Document36 pagesGreat To Have You On Board!jondraxdNo ratings yet

- MID-TERM EXAM 1 Sem 1, 2023 24 - ValuationDocument2 pagesMID-TERM EXAM 1 Sem 1, 2023 24 - Valuationphamvi44552002No ratings yet

- Midterm International Economics 2023Document4 pagesMidterm International Economics 2023Nhi Nguyễn YếnNo ratings yet

- Unit 1 Iot An Architectural Overview 1.1 Building An ArchitectureDocument43 pagesUnit 1 Iot An Architectural Overview 1.1 Building An Architecturedurvesh turbhekarNo ratings yet

- TERM PAPER of TaxationDocument25 pagesTERM PAPER of TaxationBobasa S AhmedNo ratings yet

- Formate of Business LetterDocument14 pagesFormate of Business LetterMuhammad Hamdan AfridiNo ratings yet

- Fighting Food Waste Using The Circular Economy ReportDocument40 pagesFighting Food Waste Using The Circular Economy ReportCaroline Velenthio AmansyahNo ratings yet

- Strother v. 3464920 Canada Inc.Document2 pagesStrother v. 3464920 Canada Inc.Alice JiangNo ratings yet

- Cash Flow Statements TheoryDocument16 pagesCash Flow Statements Theorysk9693092588No ratings yet

- Tribune 17th June 2023Document30 pagesTribune 17th June 2023adam shingeNo ratings yet

- CPAR 92 AUD-1st PB SolDocument3 pagesCPAR 92 AUD-1st PB SolEmmanuel TeoNo ratings yet

- Indicated in Syllabus: See Only Footnote #1: (2) Albano V. ReyesDocument1 pageIndicated in Syllabus: See Only Footnote #1: (2) Albano V. ReyesJul A.No ratings yet

- Gmail - (WWW - Dalalplus.com) Invoice ID - DLP - 57967 - 613b0770ec125Document1 pageGmail - (WWW - Dalalplus.com) Invoice ID - DLP - 57967 - 613b0770ec125Ismail Hossain Naim06132No ratings yet

- Habtamu SerteDocument17 pagesHabtamu SerteAklilu GirmaNo ratings yet

- DNV's Maritime Academy Schedule 2021 (November-December)Document2 pagesDNV's Maritime Academy Schedule 2021 (November-December)Fotini HalouvaNo ratings yet

- Proof of Residence LeaseDocument13 pagesProof of Residence Leaseapi-366174595No ratings yet

- Tenant Verification Form PDFDocument2 pagesTenant Verification Form PDFmohit kumarNo ratings yet

- 03 - Market Equlibrium and Concept of Elasticity of Demand and Its ApplicationDocument80 pages03 - Market Equlibrium and Concept of Elasticity of Demand and Its ApplicationDaksh AnejaNo ratings yet

- DIVYA VISHWAKARMA Construction IndustryDocument87 pagesDIVYA VISHWAKARMA Construction IndustryNITISH CHANDRA PANDEYNo ratings yet

- AshZjxFuEemP8Qpm209XvA Rewiring-Trade-FinanceDocument5 pagesAshZjxFuEemP8Qpm209XvA Rewiring-Trade-Financezvishavane zvishNo ratings yet

- BO - Code BO - Name BO - Add BO - Pin Div - Code Div - NameDocument20 pagesBO - Code BO - Name BO - Add BO - Pin Div - Code Div - NameSuvashreePradhan100% (1)