You might also like

- Performance-Based Road Maintenance Contracts in the CAREC RegionFrom EverandPerformance-Based Road Maintenance Contracts in the CAREC RegionNo ratings yet

- Template For Feedback On E-Vehicle Policy ConsiderationsDocument7 pagesTemplate For Feedback On E-Vehicle Policy ConsiderationssadullahNo ratings yet

- Impact of Union Budget On Capital MarketDocument29 pagesImpact of Union Budget On Capital MarketAmit DoshiNo ratings yet

- Electric Vehicles - Motivation & Overview at RIT by DR Vora 030122Document56 pagesElectric Vehicles - Motivation & Overview at RIT by DR Vora 030122Kamal VoraNo ratings yet

- Electric Two Wheeler India Market Outlook - JMK Research PDFDocument46 pagesElectric Two Wheeler India Market Outlook - JMK Research PDFAbishek Abh0% (1)

- C-ELECMOV1 - 7. Ing. Edwin Zorrilla - Electrificación de Flotas y Gestión de MicrogridsDocument40 pagesC-ELECMOV1 - 7. Ing. Edwin Zorrilla - Electrificación de Flotas y Gestión de MicrogridsEdwin AcostaNo ratings yet

- Next Genration Mobility SolutionsDocument8 pagesNext Genration Mobility SolutionsyojitNo ratings yet

- Electric Vehicle Market Nepal 2019Document10 pagesElectric Vehicle Market Nepal 2019Prajwal MaharjanNo ratings yet

- Rhb-Report-My Auto-Autoparts Sector-Update 20230117 Rhb-483379665709538263c5cdd47633e 1673939044Document8 pagesRhb-Report-My Auto-Autoparts Sector-Update 20230117 Rhb-483379665709538263c5cdd47633e 1673939044Premier Consult SolutionsNo ratings yet

- In Fa Ev Covid NoexpDocument8 pagesIn Fa Ev Covid NoexpThrishul Reddy KothapallyNo ratings yet

- Phase 1 - Build Market Confidence and Study The MarketDocument4 pagesPhase 1 - Build Market Confidence and Study The MarketAryan GargNo ratings yet

- A. Sector Information:: 1. Worldwide Contribution of Automobile Sector To The Worlds EconomyDocument6 pagesA. Sector Information:: 1. Worldwide Contribution of Automobile Sector To The Worlds EconomyFahad ParvezNo ratings yet

- Tata Motors Passenger Electric Vehicles Business: Investor Presentation 12 October 2021 Shailesh Chandra & PB BalajiDocument23 pagesTata Motors Passenger Electric Vehicles Business: Investor Presentation 12 October 2021 Shailesh Chandra & PB BalajiAshutosh RajputNo ratings yet

- Strategic Management ProjectDocument20 pagesStrategic Management ProjectMoustafa MagdyNo ratings yet

- Team Checkers: SBM, NMIMS, MumbaiDocument10 pagesTeam Checkers: SBM, NMIMS, MumbaisaurabhNo ratings yet

- EVreporter Jan 2023 MagazineDocument40 pagesEVreporter Jan 2023 MagazinemihirmmbNo ratings yet

- 6 ATRadvisorsDocument15 pages6 ATRadvisorsSiddhi KhandelwalNo ratings yet

- Maruti Suzuki - Group 8Document8 pagesMaruti Suzuki - Group 8Unnat Bharat AbhiyaanNo ratings yet

- EV Charging StationDocument21 pagesEV Charging StationVineet ChauhanNo ratings yet

- 2022 India Electric Vehicle Charging Infrastructure & Battery Swapping Market Overview ReportDocument29 pages2022 India Electric Vehicle Charging Infrastructure & Battery Swapping Market Overview ReportShehjar KaulNo ratings yet

- EV Battery PresentationDocument224 pagesEV Battery PresentationSharanappa SamalNo ratings yet

- PM Innovation ProjectDocument24 pagesPM Innovation Projecthanishgurnani 2k20umba12No ratings yet

- Decarbonising Transport PDFDocument21 pagesDecarbonising Transport PDFM.B. ConsiliandiNo ratings yet

- HSBC Investor Day 2021 PresentationDocument21 pagesHSBC Investor Day 2021 PresentationRitik UshaharaNo ratings yet

- Automotive PLI Ignores The Present Sets The Agenda For Future, ET AutoDocument20 pagesAutomotive PLI Ignores The Present Sets The Agenda For Future, ET AutoAshlesh MangrulkarNo ratings yet

- BS 6 EmissionsDocument32 pagesBS 6 EmissionsKawaljeet SinghNo ratings yet

- Renault Duster Case Study - v5Document18 pagesRenault Duster Case Study - v5Supriya BhartiNo ratings yet

- Tesalt India Private LimitedDocument16 pagesTesalt India Private LimitedSaiganesh JayakaranNo ratings yet

- Winning The Battle in The EV Ecosystem: Meta FinanceDocument34 pagesWinning The Battle in The EV Ecosystem: Meta FinanceRaghuram BathulaNo ratings yet

- FEV - BE - Electrification Trends - India - TransmissionTech - ShortDocument27 pagesFEV - BE - Electrification Trends - India - TransmissionTech - ShortNazioNo ratings yet

- Blue Minimalist Business Pitch Deck PresentationDocument19 pagesBlue Minimalist Business Pitch Deck PresentationsparkgroupnpNo ratings yet

- VAOW Pitch 22112023Document27 pagesVAOW Pitch 22112023sahilNo ratings yet

- Team: The Dependables: NMIMS, MumbaiDocument11 pagesTeam: The Dependables: NMIMS, MumbaisaurabhNo ratings yet

- Automobiles: Angels Outweighing DemonsDocument14 pagesAutomobiles: Angels Outweighing DemonsbradburywillsNo ratings yet

- Group8 Case5Document9 pagesGroup8 Case5ARYANNo ratings yet

- Ambit Money Purse Future of EV Bleak or Bright PresentaionDocument23 pagesAmbit Money Purse Future of EV Bleak or Bright PresentaionSathwikPadamNo ratings yet

- Presentation Kotak Investor Conference EVDocument24 pagesPresentation Kotak Investor Conference EVaaravNo ratings yet

- Aai Summit 02-AraiDocument26 pagesAai Summit 02-AraideipakguptaNo ratings yet

- Digital Sector Note - July 2023Document45 pagesDigital Sector Note - July 2023Lukas MullerNo ratings yet

- Apollo Tyres News - Apollo Tyres Gears Up To Meet Demand From Promising EV Segment - The Economic TimesDocument1 pageApollo Tyres News - Apollo Tyres Gears Up To Meet Demand From Promising EV Segment - The Economic TimescreateNo ratings yet

- Auto Ancillaries Revenue - 'Auto Ancillaries' Revenue May Grow 8-10% in FY23 On Stable Demand, Easing Supply-Chain Woes' - The Economic TimesDocument2 pagesAuto Ancillaries Revenue - 'Auto Ancillaries' Revenue May Grow 8-10% in FY23 On Stable Demand, Easing Supply-Chain Woes' - The Economic TimesstarNo ratings yet

- Colliers Industrial EV ReportDocument13 pagesColliers Industrial EV ReportAnandNo ratings yet

- Hand Book EV Engineering FundamentalsDocument192 pagesHand Book EV Engineering FundamentalsbhukthaNo ratings yet

- PDF&Rendition 1Document1 pagePDF&Rendition 1Monjit GogoiNo ratings yet

- Presentation 1Document7 pagesPresentation 1revantkalra2006No ratings yet

- CGD Part-1Document50 pagesCGD Part-1Vivek SinhaNo ratings yet

- LMC Automotive Global Light Vehicle Powertrain Briefing All Slides October 2020Document79 pagesLMC Automotive Global Light Vehicle Powertrain Briefing All Slides October 2020Sathya PrasadNo ratings yet

- The Road Ahead For Auto-Casting: As BS VI Emission Norms Kick in and Electric Vehicles Take OffDocument4 pagesThe Road Ahead For Auto-Casting: As BS VI Emission Norms Kick in and Electric Vehicles Take Offjignesh patilNo ratings yet

- Electric Vehicles - Lucas TVS Sets Out On A Rs 3,000-Crore Diversification Drive - The Economic TimesDocument2 pagesElectric Vehicles - Lucas TVS Sets Out On A Rs 3,000-Crore Diversification Drive - The Economic TimesstarNo ratings yet

- Automotive Industry: E2W Industry AnalysisDocument17 pagesAutomotive Industry: E2W Industry AnalysisTinsu Kumar100% (1)

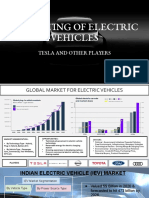

- Marketing of Electric Vehicles: Tesla and Other PlayersDocument6 pagesMarketing of Electric Vehicles: Tesla and Other PlayersKashish KhetrapalNo ratings yet

- Improving Battery Electric Vehicle Profitability FinalDocument12 pagesImproving Battery Electric Vehicle Profitability FinalsiddharthsarawgiNo ratings yet

- Advantage Rajasthan - Auto - V0.3Document11 pagesAdvantage Rajasthan - Auto - V0.3AmitNo ratings yet

- India: Performance of Electric Vehicle Industry: Quarterly Update: Q1 FY 2021 (Apr'2020 - Jun'2020)Document10 pagesIndia: Performance of Electric Vehicle Industry: Quarterly Update: Q1 FY 2021 (Apr'2020 - Jun'2020)SoundararajanNo ratings yet

- LPEM-UI - Study Report LPEM 8 August 2018 + Key M v6 0Document41 pagesLPEM-UI - Study Report LPEM 8 August 2018 + Key M v6 0Muhammad Ma'rufNo ratings yet

- Small Engines: Global Motorcycle Trends E-Mobility Trends Emissions Legislation Upgrades Motorcycle MarketDocument8 pagesSmall Engines: Global Motorcycle Trends E-Mobility Trends Emissions Legislation Upgrades Motorcycle MarketJahmia CoralieNo ratings yet

- E-Mobility in INDIA Challenges and Opportunities: Presented by Dr. Vikram KumarDocument90 pagesE-Mobility in INDIA Challenges and Opportunities: Presented by Dr. Vikram KumarBharath Raj100% (1)

- Ptmail - m1021 - Ss - Ev Ultimate Market Intelligence ReportDocument23 pagesPtmail - m1021 - Ss - Ev Ultimate Market Intelligence ReportPIYUSH GOPALNo ratings yet

- Dr. Ashok Jhunjhunwala IIT MadrasDocument10 pagesDr. Ashok Jhunjhunwala IIT Madrasjoycool100% (1)

- Final Presentaton - Group 2050Document23 pagesFinal Presentaton - Group 2050Jasleen KaurNo ratings yet

- Groww Digest - 28 July 2021Document8 pagesGroww Digest - 28 July 2021Tejesh GoudNo ratings yet

- Groww Digest - 02 August 2021Document8 pagesGroww Digest - 02 August 2021Tejesh GoudNo ratings yet

- What Is Happening With The API Companies?Document23 pagesWhat Is Happening With The API Companies?Tejesh GoudNo ratings yet

- AGS Transact Technologies LTD - IPO Note - Jan'2022Document10 pagesAGS Transact Technologies LTD - IPO Note - Jan'2022Tejesh GoudNo ratings yet

- IS Ev Ready?: Anish Moonka, Head of Research, JST InvestmentsDocument30 pagesIS Ev Ready?: Anish Moonka, Head of Research, JST InvestmentsTejesh GoudNo ratings yet

- Globus SpiritsDocument5 pagesGlobus SpiritsTejesh GoudNo ratings yet

- Globus Con CallDocument15 pagesGlobus Con CallTejesh GoudNo ratings yet

- Automobiles SectorDocument45 pagesAutomobiles SectorTejesh GoudNo ratings yet

- HDFC MF Yearbook 2022Document88 pagesHDFC MF Yearbook 2022Tejesh GoudNo ratings yet

- IPO Diary Feb'2022Document89 pagesIPO Diary Feb'2022Tejesh GoudNo ratings yet

- Jefferies On Metal StocksDocument36 pagesJefferies On Metal StocksTejesh GoudNo ratings yet

- Adani Wilmar Limited IpoDocument19 pagesAdani Wilmar Limited IpoTejesh GoudNo ratings yet

- Globus SpiritsDocument17 pagesGlobus SpiritsTejesh GoudNo ratings yet

- ANTONY WASTE HSL Initiating Coverage 190122Document17 pagesANTONY WASTE HSL Initiating Coverage 190122Tejesh GoudNo ratings yet

- Ece Er 22, 2 ST Epar e Natio A Stock Exchange Complex, Bandra East), 400 Symbol Zeel Eq Zeel P2Document8 pagesEce Er 22, 2 ST Epar e Natio A Stock Exchange Complex, Bandra East), 400 Symbol Zeel Eq Zeel P2Tejesh GoudNo ratings yet

- National Stock Exchange of India Limited BSE LimitedDocument2 pagesNational Stock Exchange of India Limited BSE LimitedTejesh GoudNo ratings yet

- India - Infra SectorDocument199 pagesIndia - Infra SectorTejesh GoudNo ratings yet

- INDIAN HOTELS - Initiating CoverageDocument30 pagesINDIAN HOTELS - Initiating CoverageTejesh GoudNo ratings yet

- Latent View - Intimation of Anchor AllocationDocument6 pagesLatent View - Intimation of Anchor AllocationTejesh GoudNo ratings yet

- Paytm by MacquarieDocument8 pagesPaytm by MacquarieTejesh GoudNo ratings yet

- Top Picks - Axis-November2021Document79 pagesTop Picks - Axis-November2021Tejesh GoudNo ratings yet

- Cement Small Caps: House Is in Order Small Caps Ripe For Re-RatingDocument48 pagesCement Small Caps: House Is in Order Small Caps Ripe For Re-RatingTejesh GoudNo ratings yet

- Paytm - Anchor AllocationDocument10 pagesPaytm - Anchor AllocationTejesh GoudNo ratings yet

- Red Herring ProspectusDocument414 pagesRed Herring ProspectusTejesh GoudNo ratings yet

- Heranba - Initiating CoverageDocument33 pagesHeranba - Initiating CoverageTejesh GoudNo ratings yet

- Mercedes SLS AmgDocument35 pagesMercedes SLS AmgNavdeep MayallNo ratings yet

- April 3 Approval of Bill On Tax Breaks Will Pave Way For Widespread Use of Hybrid CarsDocument1 pageApril 3 Approval of Bill On Tax Breaks Will Pave Way For Widespread Use of Hybrid Carspribhor2No ratings yet

- Hykangoo Uk2013Document2 pagesHykangoo Uk2013HasanUSLUMNo ratings yet

- Route Map Bus Times: ServiceDocument2 pagesRoute Map Bus Times: ServiceGrimmo1979No ratings yet

- Higuey, Dom Rep Mdpc/Puj: .Eff.23.MayDocument5 pagesHiguey, Dom Rep Mdpc/Puj: .Eff.23.MayVanessa Yumayusa0% (1)

- Mercantil Incident ReportDocument3 pagesMercantil Incident ReportG06 ELARDO, Trish F.No ratings yet

- Lecture 2Document31 pagesLecture 2prekshabNo ratings yet

- GM Business PlanDocument6 pagesGM Business PlanPriyanka NemaNo ratings yet

- Sharan Electrical SystemDocument258 pagesSharan Electrical SystemGilbert SpariosNo ratings yet

- LHD Toro0010 (13 Yd3) PDFDocument2 pagesLHD Toro0010 (13 Yd3) PDFDaniel LopezNo ratings yet

- Automobile February 2023Document29 pagesAutomobile February 2023Hymad RajakNo ratings yet

- Standardized Training Packages (STPS) CatalogueDocument107 pagesStandardized Training Packages (STPS) CatalogueJoão AlmeidaNo ratings yet

- 211-02 Power Steering - Removal and Installation - Steering Gear 4WDDocument7 pages211-02 Power Steering - Removal and Installation - Steering Gear 4WDCARLOS LIMADANo ratings yet

- Jordan Airspace ManualDocument11 pagesJordan Airspace ManualA320viatorNo ratings yet

- Jack Jameson ResumeDocument3 pagesJack Jameson ResumeamerajackNo ratings yet

- 021 Crane Operator ChecklistDocument1 page021 Crane Operator ChecklistJunard Lu HapNo ratings yet

- TK50CF Trailer Owner's Manual 46 OffDocument52 pagesTK50CF Trailer Owner's Manual 46 Offwilson chaconNo ratings yet

- Airframe Structures - Term II - 2016 Module 1 (Y1 A&E and AVI)Document3 pagesAirframe Structures - Term II - 2016 Module 1 (Y1 A&E and AVI)ACLINNo ratings yet

- Two Post Lift: Rhino 3.2 LDocument1 pageTwo Post Lift: Rhino 3.2 LviahulNo ratings yet

- Delta TechOps Cababilities OverviewDocument26 pagesDelta TechOps Cababilities Overviewjoaco91No ratings yet

- Case Study ON Laxmi TransformersDocument10 pagesCase Study ON Laxmi TransformersAjay BorichaNo ratings yet

- Chapter 1 Vehicle Dynamics and Control 2015 Vehicle Handling Dynamics Second EditionDocument3 pagesChapter 1 Vehicle Dynamics and Control 2015 Vehicle Handling Dynamics Second EditionKunheechoNo ratings yet

- Product Recommendation Caterpillar Forklift Trucks, Diesel V225B PDFDocument2 pagesProduct Recommendation Caterpillar Forklift Trucks, Diesel V225B PDFConnie RodriguezNo ratings yet

- CTU Code January 2014 PDFDocument129 pagesCTU Code January 2014 PDFJavierContiNo ratings yet

- Report - WPR20CA125 - 101176 - 7232022 83819 AMDocument5 pagesReport - WPR20CA125 - 101176 - 7232022 83819 AMKhan RihanNo ratings yet

- Model 112 Rigid AxleDocument2 pagesModel 112 Rigid AxlePrasad100% (1)

- Basic Naval Architecture - Ship Stability (PDFDrive) - Pages-20-33Document14 pagesBasic Naval Architecture - Ship Stability (PDFDrive) - Pages-20-33veryawan nanda perkasaNo ratings yet

- DerbyCityCouncil Wizquiz Presentation PDFDocument123 pagesDerbyCityCouncil Wizquiz Presentation PDFShubham NamdevNo ratings yet

- Dedicated To Excellence: Ponsse OyjDocument8 pagesDedicated To Excellence: Ponsse OyjkeesNo ratings yet

- Paper 4 Final DraftDocument5 pagesPaper 4 Final Draftapi-665151630No ratings yet