You might also like

- Business Combination - Stock AcquisitionDocument6 pagesBusiness Combination - Stock AcquisitionEmma Mariz GarciaNo ratings yet

- Group Accounts - Subsidiaries (CSOFP) : Chapter Learning ObjectivesDocument58 pagesGroup Accounts - Subsidiaries (CSOFP) : Chapter Learning ObjectivesKeotshepile Esrom MputleNo ratings yet

- Principles of Consolidated Financial Statements: 1 The Concept of Group AccountsDocument58 pagesPrinciples of Consolidated Financial Statements: 1 The Concept of Group Accountssagar khadkaNo ratings yet

- AP 03 - REO Shareholders - Equity2Document10 pagesAP 03 - REO Shareholders - Equity2jeshiela mae biloNo ratings yet

- 3 Group Accounts and Business Combinations Lecture NotesDocument47 pages3 Group Accounts and Business Combinations Lecture NotesAKINYEMI ADISA KAMORU100% (4)

- Investment in AssociateDocument60 pagesInvestment in Associateadarose romaresNo ratings yet

- Responsibility AccountingDocument3 pagesResponsibility AccountingMilcah Deloso SantosNo ratings yet

- Investment in AssocociateDocument10 pagesInvestment in AssocociateShaina SamonteNo ratings yet

- CA. Ranjay Mishra (FCA)Document14 pagesCA. Ranjay Mishra (FCA)ZamanNo ratings yet

- Consolidated Statement of Financial PositionDocument6 pagesConsolidated Statement of Financial PositionRameen FatimaNo ratings yet

- Group Accounts - Subsidiaries (CSPLOCI) : Chapter Learning ObjectivesDocument28 pagesGroup Accounts - Subsidiaries (CSPLOCI) : Chapter Learning ObjectivesKeotshepile Esrom MputleNo ratings yet

- Investments For Investments in Equity Securities (Shares)Document2 pagesInvestments For Investments in Equity Securities (Shares)Carms St ClaireNo ratings yet

- Basic Consol Acc2 & 3Document17 pagesBasic Consol Acc2 & 3fortuinpdNo ratings yet

- ACCA SBR Workbook 2018 Errata SheetDocument8 pagesACCA SBR Workbook 2018 Errata SheetdeltaeagleNo ratings yet

- Summary of EliminationsDocument7 pagesSummary of EliminationsSella DestikaNo ratings yet

- FAR 15 Investment in AssociatesDocument2 pagesFAR 15 Investment in AssociatesShaira Mae DausNo ratings yet

- Review of Financial Statement Preparation Lecture NotesDocument4 pagesReview of Financial Statement Preparation Lecture Noteslashy123booNo ratings yet

- The Consolidated Statement of Financial Position (Formerly Known As Consolidated Balance Sheet-CBS)Document5 pagesThe Consolidated Statement of Financial Position (Formerly Known As Consolidated Balance Sheet-CBS)illyanaNo ratings yet

- AUDIT OF INVESTMENTS - AssociateDocument4 pagesAUDIT OF INVESTMENTS - AssociateJoshua LisingNo ratings yet

- Consolidated Financial AccountingDocument3 pagesConsolidated Financial AccountingEmma Mariz GarciaNo ratings yet

- Ias 1Document7 pagesIas 1ADEYANJU AKEEMNo ratings yet

- Notes Chapter 3 FARDocument4 pagesNotes Chapter 3 FARcpacfa100% (7)

- 6 - Consolidated Financial Statements P2 PDFDocument5 pages6 - Consolidated Financial Statements P2 PDFDarlene Faye Cabral RosalesNo ratings yet

- Revision Notes Group Accounts PDFDocument11 pagesRevision Notes Group Accounts PDFEhsanulNo ratings yet

- AFR Revision - Qns-AnsDocument63 pagesAFR Revision - Qns-AnsDownloder UwambajimanaNo ratings yet

- 5.consolidated SOCI - AAFRDocument11 pages5.consolidated SOCI - AAFRAli OptimisticNo ratings yet

- 04 Group Financial StatementsDocument56 pages04 Group Financial StatementsHaris IshaqNo ratings yet

- Financial Statements of A PartnershipDocument12 pagesFinancial Statements of A PartnershipCharlesNo ratings yet

- Summary of Basic Conso TechniquesDocument5 pagesSummary of Basic Conso Techniquesutary4s3No ratings yet

- Financial Statement AnalysisDocument46 pagesFinancial Statement AnalysisMusom BBANo ratings yet

- 3rd Sem AccountsDocument67 pages3rd Sem Accountsharamilanda2004No ratings yet

- LeveragesDocument9 pagesLeveragesShrinivasan IyengarNo ratings yet

- Alternative Treatment To SLPSAS 11 - Addendum To SLPSAS Volume IIIDocument4 pagesAlternative Treatment To SLPSAS 11 - Addendum To SLPSAS Volume IIIgeethNo ratings yet

- IFRS Notes December 2021Document12 pagesIFRS Notes December 2021AnnaNo ratings yet

- CFAP1+ +Study+Manual+ 67Document1 pageCFAP1+ +Study+Manual+ 67.No ratings yet

- Ias 28 AssociateDocument19 pagesIas 28 AssociateĐức DuyNo ratings yet

- CSEC English A 2023 P2 - 230111 - 163228 PDFDocument7 pagesCSEC English A 2023 P2 - 230111 - 163228 PDF27h4fbvsy8No ratings yet

- Formats For Consolidation Group StructureDocument4 pagesFormats For Consolidation Group StructureMuhammad3588No ratings yet

- CONSOLIDATIONDocument21 pagesCONSOLIDATIONVaishnavi ChaturvediNo ratings yet

- Ratio Analysis Theory and ProblemsDocument13 pagesRatio Analysis Theory and ProblemsPunit Kuleria100% (1)

- Joint ArrangementsDocument9 pagesJoint Arrangementscarlos antonio IbuanNo ratings yet

- Topic 6 Partnership: 6.1 FormationDocument5 pagesTopic 6 Partnership: 6.1 FormationxxpjulxxNo ratings yet

- Acc407 CH7 PartnershipDocument26 pagesAcc407 CH7 PartnershipBATRISYIA AMANI MUHAMMAD HALIMNo ratings yet

- Question 2 Single Company AccountsDocument10 pagesQuestion 2 Single Company AccountsjbmggknbrxNo ratings yet

- Insolvency of PartnersDocument1 pageInsolvency of PartnersshabukrNo ratings yet

- BEACTG 03 REVISED MODULE 8 Components of Stockholder's Equity of Different Forms of Business OwnershipDocument7 pagesBEACTG 03 REVISED MODULE 8 Components of Stockholder's Equity of Different Forms of Business OwnershipJessica PangilinanNo ratings yet

- Consolidated Financial StatementsDocument27 pagesConsolidated Financial StatementsAlyssa CasimiroNo ratings yet

- Intermediate Accounting - Investment in Associate (Pas 28)Document3 pagesIntermediate Accounting - Investment in Associate (Pas 28)22100629No ratings yet

- Financial Statements PDFDocument14 pagesFinancial Statements PDFArik HassanNo ratings yet

- Bcom PPT 4Document22 pagesBcom PPT 4dmangiginNo ratings yet

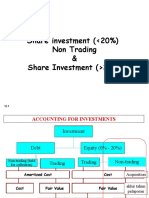

- 12.2 Share Investment Non Trading & Share Invesment Lebih 20%Document18 pages12.2 Share Investment Non Trading & Share Invesment Lebih 20%TIFFANNY SHELIANo ratings yet

- Statement of Cash Flows (IAS 7) : Reconciliation of Operating Profit To Net Cash Flow From OperationsDocument2 pagesStatement of Cash Flows (IAS 7) : Reconciliation of Operating Profit To Net Cash Flow From OperationspriyaNo ratings yet

- SHAREHOLDERSDocument13 pagesSHAREHOLDERSJanisseNo ratings yet

- Corporate Unit 3Document497 pagesCorporate Unit 3bhavu aryaNo ratings yet

- Business Finance Week 4 To 5 Without AnswerDocument13 pagesBusiness Finance Week 4 To 5 Without AnswerKristel Anne Roquero BalisiNo ratings yet

- The Formulas of All The Ratios: A. Financial Stability, Solvency, Liquidity, Balance Sheet RatiosDocument2 pagesThe Formulas of All The Ratios: A. Financial Stability, Solvency, Liquidity, Balance Sheet RatiosAayush AgrawalNo ratings yet

- Chapter 9 - BondsDocument6 pagesChapter 9 - BondsGABBY NACA STEVANYNo ratings yet

- Financial Statement Analysis & Ratio AnalysisDocument21 pagesFinancial Statement Analysis & Ratio Analysissriharsha5877454No ratings yet

- ASFDDocument1 pageASFD.No ratings yet

- ASFDDocument1 pageASFD.No ratings yet

- ASFDDocument1 pageASFD.No ratings yet

- ASFDDocument1 pageASFD.No ratings yet

- ASFDDocument1 pageASFD.No ratings yet

- Dear Shareholders,: Future OutlookDocument1 pageDear Shareholders,: Future Outlook.No ratings yet

- ASFDDocument1 pageASFD.No ratings yet

- Profile of The Board: Syed Bakhtiyar KazmiDocument1 pageProfile of The Board: Syed Bakhtiyar Kazmi.No ratings yet

- Major Gen Naseer Ali Khan: ST SC HR EC SIC ACDocument1 pageMajor Gen Naseer Ali Khan: ST SC HR EC SIC AC.No ratings yet

- ASFDDocument1 pageASFD.No ratings yet

- ASFDDocument1 pageASFD.No ratings yet

- 2022 Performance Highlights: People Planet ProsperityDocument1 page2022 Performance Highlights: People Planet Prosperity.No ratings yet

- Syed Atif Ali: ST HR SIC AC SC ECDocument1 pageSyed Atif Ali: ST HR SIC AC SC EC.No ratings yet

- Company Directors' SustainabilityDocument1 pageCompany Directors' Sustainability.No ratings yet

- DFSDDocument1 pageDFSD.No ratings yet

- Financial CapitalDocument1 pageFinancial Capital.No ratings yet

- DsasDocument1 pageDsas.No ratings yet

- Workings Rs.000Document1 pageWorkings Rs.000.No ratings yet

- Al - 62Document1 pageAl - 62.No ratings yet

- The Grape Group (Acquisition) : Cfap 1: A A F RDocument1 pageThe Grape Group (Acquisition) : Cfap 1: A A F R.No ratings yet

- Chap 16 - Capital Structure - Basic ConceptsDocument37 pagesChap 16 - Capital Structure - Basic ConceptsAdiba IbnatNo ratings yet

- Nishat Cash FlowDocument2 pagesNishat Cash FlowomairNo ratings yet

- A.1. Financial Statements Part 2Document53 pagesA.1. Financial Statements Part 2Kondreddi SakuNo ratings yet

- Module 5 - Cost of CapitalDocument5 pagesModule 5 - Cost of Capitaljay-ar dimaculanganNo ratings yet

- M&A NotesDocument22 pagesM&A NotesБота ОмароваNo ratings yet

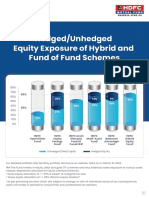

- Leaflet - Hedged and Unhedged Exposure of Hybrid FundsDocument2 pagesLeaflet - Hedged and Unhedged Exposure of Hybrid FundsDeepakNo ratings yet

- Investment Decision RulesDocument7 pagesInvestment Decision RulesQuỳnh Anh TrầnNo ratings yet

- CAIIB ABFM Module B Mini Marathon 2Document21 pagesCAIIB ABFM Module B Mini Marathon 2Nandagopal KannanNo ratings yet

- Far210 - July2020 SS Q5Document2 pagesFar210 - July2020 SS Q5imn njwaaaNo ratings yet

- ITC Financial ModelDocument150 pagesITC Financial ModelKaushik JainNo ratings yet

- Capital Asset Pricing ModelDocument10 pagesCapital Asset Pricing Modeljackie555No ratings yet

- Công ty Cổ Phần Vàng Bạc Đá Quý Phú Nhuận (PNJ)Document15 pagesCông ty Cổ Phần Vàng Bạc Đá Quý Phú Nhuận (PNJ)Thảo MaiNo ratings yet

- FinRep SummaryDocument36 pagesFinRep SummaryNikolaNo ratings yet

- Tutorial 7 - (Solution) Analysis of Financial StatementsDocument4 pagesTutorial 7 - (Solution) Analysis of Financial StatementsSamer LaabidiNo ratings yet

- Week 11 In-Class Exercise (Topic 9) - WORKSHEETDocument4 pagesWeek 11 In-Class Exercise (Topic 9) - WORKSHEETDương LêNo ratings yet

- CH10 ProblemDocument1 pageCH10 ProblemTrần Hoàng Thành DươngNo ratings yet

- Fundamentals of Corporate Finance 12th Edition Ross Test BankDocument35 pagesFundamentals of Corporate Finance 12th Edition Ross Test Bankadeliahue1q9kl100% (19)

- 5 Books Recommended by Paul Tudor JonesDocument4 pages5 Books Recommended by Paul Tudor Jonesjackhack220No ratings yet

- Solution To Quiz 1Document10 pagesSolution To Quiz 1HUANG WENCHENNo ratings yet

- SQB 1017020Document290 pagesSQB 1017020Екатерина ПетроваNo ratings yet

- 33 Investment StrategiesDocument9 pages33 Investment StrategiesAani RashNo ratings yet

- Ravi Kishore BookDocument3 pagesRavi Kishore BookZeeshan Sikandar0% (1)

- Dec 2022 - Strategic Financial ManagementDocument8 pagesDec 2022 - Strategic Financial ManagementindrakumarNo ratings yet

- 2016 Fund Industry in LuxembourgDocument104 pages2016 Fund Industry in LuxembourgShtutz IlianNo ratings yet

- Mutual Fund Report Jun-19Document45 pagesMutual Fund Report Jun-19muddasir1980No ratings yet

- B326 TMA 23-24 (Fall) V1Document5 pagesB326 TMA 23-24 (Fall) V1adel.dahbour9733% (3)

- Oacc - Pp&e P 1 - P3Document23 pagesOacc - Pp&e P 1 - P3Trixie Divine SantosNo ratings yet

- Accounting Last Push-GautengDocument26 pagesAccounting Last Push-GautengYolisa NkosiNo ratings yet

- AdmissionDocument23 pagesAdmissionPawan TalrejaNo ratings yet

- ACC3210Document6 pagesACC3210anba velooNo ratings yet