You might also like

- 1905 - 2 - Faraj Al AmmariDocument48 pages1905 - 2 - Faraj Al AmmariAbdulhakim TREKINo ratings yet

- Rebuilding Trust and Mainstreaming Renewable EnergyDocument20 pagesRebuilding Trust and Mainstreaming Renewable EnergyyaksmartNo ratings yet

- Smart Grid in TransmissionDocument26 pagesSmart Grid in TransmissionAEE 400KVNo ratings yet

- Lecture 13Document34 pagesLecture 13kamran bhatNo ratings yet

- 1 HVDC Systems in IndiaDocument45 pages1 HVDC Systems in IndiaAniket BabutaNo ratings yet

- 5.2. Pakistan Country Presentation by A. AllaudinDocument24 pages5.2. Pakistan Country Presentation by A. Allaudinquantum_leap_windNo ratings yet

- Solar Thermal Power GenerationDocument101 pagesSolar Thermal Power GenerationAvnish Narula100% (5)

- Loading of important EHV elements during April-June 2020Document2 pagesLoading of important EHV elements during April-June 2020Pranay PatelNo ratings yet

- Atomic ReactorsDocument128 pagesAtomic ReactorslucinipeNo ratings yet

- The Tata Power Company Limited: Analyst Meet - March 2008Document65 pagesThe Tata Power Company Limited: Analyst Meet - March 2008yoursmathew22No ratings yet

- Renewable Integration - POWERGRIDDocument29 pagesRenewable Integration - POWERGRIDvaibhav bodkheNo ratings yet

- Sanjid Vai EEE Syllabus PDFDocument27 pagesSanjid Vai EEE Syllabus PDFSakib HossainNo ratings yet

- Solar Power Project-200 KVA Roof TopDocument22 pagesSolar Power Project-200 KVA Roof TopRajesh ThulluriNo ratings yet

- Edc Power Plant FacilitiesDocument32 pagesEdc Power Plant FacilitiesMichael TayactacNo ratings yet

- TN 50543 03-16-09 Electric Transmission-Related Data SubmittalDocument46 pagesTN 50543 03-16-09 Electric Transmission-Related Data Submittalreza ashtariNo ratings yet

- Power Project Corrected Question Answers Class 8Document6 pagesPower Project Corrected Question Answers Class 8Piyush RajNo ratings yet

- Delhi Metro Power TransmissionDocument13 pagesDelhi Metro Power Transmission2K18/EE/026 ANGAD SINGH NAGINo ratings yet

- MERALCO's Proposed Malacafiang 115 kV-34.5 kV GIS Substation ProjectDocument101 pagesMERALCO's Proposed Malacafiang 115 kV-34.5 kV GIS Substation ProjectMark Ivan JagodillaNo ratings yet

- TAIKAI Group-CompressedDocument27 pagesTAIKAI Group-CompressedGV TNo ratings yet

- Lecture 1 Power Flow ControlDocument54 pagesLecture 1 Power Flow ControlSidharth MishraNo ratings yet

- Appendix "A": 12.5 MW Biomass PP Roman Superhighway, Brgy. Gugo, Samal, BataanDocument5 pagesAppendix "A": 12.5 MW Biomass PP Roman Superhighway, Brgy. Gugo, Samal, BataanrajgonzNo ratings yet

- Boiler Water ChemistryDocument36 pagesBoiler Water ChemistrySami ZiaNo ratings yet

- Chellapandi CoSS2015 KeynoteDocument53 pagesChellapandi CoSS2015 KeynoteArunprasad MurugesanNo ratings yet

- Power Stations Run by Steam Turbine in Bangladesh: Answer To The Question No-Q.5Document6 pagesPower Stations Run by Steam Turbine in Bangladesh: Answer To The Question No-Q.5Nabil AbdullahNo ratings yet

- Former Power Secretary PresentationDocument37 pagesFormer Power Secretary PresentationMasuk HasanNo ratings yet

- Luzon Power Outlook BriefingDocument28 pagesLuzon Power Outlook BriefingrestigabuyaNo ratings yet

- Rajiv Mishra-India - Pakistan Energy Cooperation - 30.01.2015Document14 pagesRajiv Mishra-India - Pakistan Energy Cooperation - 30.01.2015Utkarsh BenjwalNo ratings yet

- Final Hoody.1Document81 pagesFinal Hoody.1muslimwaqar2002No ratings yet

- Iloilo Energy 101 05 Power 101Document27 pagesIloilo Energy 101 05 Power 101allanNo ratings yet

- Myanmar's Electricity Sector StatusDocument27 pagesMyanmar's Electricity Sector Status정상진100% (1)

- Introduction Indian PsDocument15 pagesIntroduction Indian PsRavinder SharmaNo ratings yet

- 2007 Tang (ABB)Document27 pages2007 Tang (ABB)Olga SuslovaNo ratings yet

- Iraq's Natural Gas Challenge for Electricity GenerationDocument21 pagesIraq's Natural Gas Challenge for Electricity GenerationShameer Majeed. ANo ratings yet

- JPS35-395 - Lead Acid Batteries in Utility Energy Storage AnDocument4 pagesJPS35-395 - Lead Acid Batteries in Utility Energy Storage Ancarlosalberto.camargoNo ratings yet

- References_FZSoNickDocument1 pageReferences_FZSoNickVerde GriNo ratings yet

- SCEPresentation 2022 2023TransmissionPlanningProcess Sep28 2022Document22 pagesSCEPresentation 2022 2023TransmissionPlanningProcess Sep28 2022arjeegeeNo ratings yet

- Electricity in PakistanDocument22 pagesElectricity in Pakistanglamoure100% (1)

- 1 HVDC Systems in India PDFDocument45 pages1 HVDC Systems in India PDFSrinivas ReddyNo ratings yet

- 765/400kV SLD and Asset DetailsDocument42 pages765/400kV SLD and Asset DetailssadegaonkarNo ratings yet

- Book 1Document78 pagesBook 1kinshuksingh.0798No ratings yet

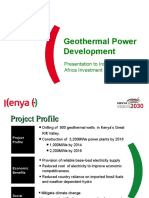

- Geothermal Power Development: Presentation To Institutional Investor Africa Investment ConferenceDocument16 pagesGeothermal Power Development: Presentation To Institutional Investor Africa Investment ConferenceKenya Ict BoardNo ratings yet

- WEG EPC Solar PresentationDocument31 pagesWEG EPC Solar PresentationHADJENE NoussaibaNo ratings yet

- 167206180294status of Margins Available at Existing ISTS - 30!11!2022 - RevDocument10 pages167206180294status of Margins Available at Existing ISTS - 30!11!2022 - RevVaibhav KapoorNo ratings yet

- Renewable - Resources - and - Potentials - 20.12.2016 Ministry of PowerDocument32 pagesRenewable - Resources - and - Potentials - 20.12.2016 Ministry of Powernana yawNo ratings yet

- IDOM Power Grid and I&E UK ReferencesDocument64 pagesIDOM Power Grid and I&E UK ReferencesFaustino Guillén MinguitoNo ratings yet

- Prospects of Renewable Energy in PakistanDocument34 pagesProspects of Renewable Energy in PakistanADBI EventsNo ratings yet

- Energy Utilities Sector StudyDocument3 pagesEnergy Utilities Sector Studycmverma82No ratings yet

- Introduction to Grid Station OperationDocument99 pagesIntroduction to Grid Station OperationSher AliNo ratings yet

- ch-1 INTRODUCTION PDFDocument10 pagesch-1 INTRODUCTION PDFBhavin ShahNo ratings yet

- The Crucial Role of Natural Gas and LNG For Power in BangladeshDocument19 pagesThe Crucial Role of Natural Gas and LNG For Power in BangladeshLNG Cell PetrobanglaNo ratings yet

- Chapter 3Document16 pagesChapter 3manasb6342No ratings yet

- Power Plant IntroductionDocument15 pagesPower Plant IntroductionBlackNo ratings yet

- Status of Myanmar Electric Power and Hydropower PlanningDocument18 pagesStatus of Myanmar Electric Power and Hydropower PlanningTHAN HANNo ratings yet

- Detailed Project Report For Transmission System For Solar Power Parks at Bhadla, RajasthanDocument58 pagesDetailed Project Report For Transmission System For Solar Power Parks at Bhadla, RajasthanAbhinav TamrakarNo ratings yet

- List of Important Grid Elements - ER - 2023 - MayDocument56 pagesList of Important Grid Elements - ER - 2023 - Maysiddhesh.chaudhariNo ratings yet

- Figure 1 - Leyte-Luzon HVDC Transmission ProjectDocument8 pagesFigure 1 - Leyte-Luzon HVDC Transmission ProjectDånøèSåpütråNo ratings yet

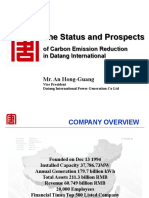

- The Status and ProspectsDocument13 pagesThe Status and ProspectskmozoaNo ratings yet

- Advances in High Voltage Insulation and Arc Interruption in SF6 and VacuumFrom EverandAdvances in High Voltage Insulation and Arc Interruption in SF6 and VacuumNo ratings yet

- Electromechanical Energy Conversion PrinciplesDocument5 pagesElectromechanical Energy Conversion PrinciplesVastie RozulNo ratings yet

- Types and Characteristics of DC GeneratorDocument9 pagesTypes and Characteristics of DC GeneratorVastie RozulNo ratings yet

- DOE List of Existing Luzon Grid Power Plants as of June 2018Document4 pagesDOE List of Existing Luzon Grid Power Plants as of June 2018jodhusNo ratings yet

- Power Development Plan 2016-2040 PDFDocument93 pagesPower Development Plan 2016-2040 PDFEmman Joshua BustoNo ratings yet

- Energy Demand On 2040 PDFDocument57 pagesEnergy Demand On 2040 PDFVastie RozulNo ratings yet

- DDP 2016-2025Document190 pagesDDP 2016-2025Marjoerie CasteloNo ratings yet

- Doe - Energy Demand and Supply Outlook PDFDocument46 pagesDoe - Energy Demand and Supply Outlook PDFVastie RozulNo ratings yet

- DOE PRESENTATION ON PHILIPPINES ENERGY SITUATION AND OUTLOOKDocument55 pagesDOE PRESENTATION ON PHILIPPINES ENERGY SITUATION AND OUTLOOKmltobias_826283323No ratings yet

- Power Plant Engineering AssignmentDocument2 pagesPower Plant Engineering AssignmentVastie RozulNo ratings yet

- 2017 Philippine power demand and supply highlightsDocument107 pages2017 Philippine power demand and supply highlightsVastie RozulNo ratings yet

- Sample of Hazardous Area ClassificationDocument35 pagesSample of Hazardous Area ClassificationMouath AlraoushNo ratings yet

- LPG in World Markets Jan 2016 PDFDocument32 pagesLPG in World Markets Jan 2016 PDFJcoveNo ratings yet

- Definitions - Upstream, Midstream and DownstreamDocument17 pagesDefinitions - Upstream, Midstream and DownstreammagveyNo ratings yet

- Industry Insights: Equity ResearchDocument31 pagesIndustry Insights: Equity ResearchDanielNo ratings yet

- Decarbonisation of Steam CrackersDocument7 pagesDecarbonisation of Steam CrackersAtharva OfficeNo ratings yet

- Types of Stations in CGDDocument49 pagesTypes of Stations in CGDSHOBHIT KUMAR0% (1)

- Thesis Topics For Renewable EnergyDocument4 pagesThesis Topics For Renewable Energyheatherleeseattle100% (2)

- Campus Proposal GETDocument2 pagesCampus Proposal GETAmogha kantakNo ratings yet

- Ec96 53Document31 pagesEc96 53tinashemambarizaNo ratings yet

- LNG Weathering - Data DropDocument21 pagesLNG Weathering - Data DropMoch FaridNo ratings yet

- Sdewes 2019Document737 pagesSdewes 2019renata portelaNo ratings yet

- Coal and Petroleum (Notes) - Version 2.0-1Document8 pagesCoal and Petroleum (Notes) - Version 2.0-1Akshat OberoiNo ratings yet

- CHE 422 Fall 2021 L1Document11 pagesCHE 422 Fall 2021 L1Zain Gillani100% (1)

- Selecting of Vaporizer in LNG Regasification Plant: M. Ebrahimi Gardeshi, M. A. ShobeiriDocument7 pagesSelecting of Vaporizer in LNG Regasification Plant: M. Ebrahimi Gardeshi, M. A. ShobeiriundungNo ratings yet

- Kazakh CrudeDocument11 pagesKazakh CrudeValentinoIgosevNo ratings yet

- CH 5 Coal and PetroleumDocument2 pagesCH 5 Coal and PetroleumYASHVI MODINo ratings yet

- From Russia With Gas An Analysis of The Nord StreaDocument19 pagesFrom Russia With Gas An Analysis of The Nord StreaDImiskoNo ratings yet

- GlobalHydrogenReview 2022-12Document72 pagesGlobalHydrogenReview 2022-12jmod7867No ratings yet

- JujerumisagoxonukadDocument3 pagesJujerumisagoxonukadLekhotla SibayaNo ratings yet

- Compressor Tech2 - October 2022Document54 pagesCompressor Tech2 - October 2022PericoNo ratings yet

- Alistair SmithDocument13 pagesAlistair SmithRASHID AHMED SHAIKHNo ratings yet

- Non Renewable EnergyDocument59 pagesNon Renewable EnergyMelbertNo ratings yet

- ANovel Designof Liquefied Natural Gas LNGRegasification Power Plant Integratedwith Cryogenic Energy Storage SystemDocument9 pagesANovel Designof Liquefied Natural Gas LNGRegasification Power Plant Integratedwith Cryogenic Energy Storage SystemTala RamezaniNo ratings yet

- Properties of LNGDocument2 pagesProperties of LNGdillooseNo ratings yet

- Casing TypesDocument13 pagesCasing Typeshardik khandelwal100% (3)

- Average Market Capitalizationoflistedcompaniesduringthesixmonthsended 31 Dec 2023Document84 pagesAverage Market Capitalizationoflistedcompaniesduringthesixmonthsended 31 Dec 2023Nirvana BoyNo ratings yet

- Fire and Gas System in Oil and GasDocument59 pagesFire and Gas System in Oil and GasGiftObionochieNo ratings yet

- Oil and Gas 101: An Overview of Oil and Gas Upstream Activities, Regulations, and Emission InventoriesDocument120 pagesOil and Gas 101: An Overview of Oil and Gas Upstream Activities, Regulations, and Emission InventoriesramyNo ratings yet

- Lesson 8: Fuels and Grease Flash and Fire Points of Liquid Fuels and GreaseDocument19 pagesLesson 8: Fuels and Grease Flash and Fire Points of Liquid Fuels and GreaseBernadette BoncolmoNo ratings yet

- Indian Oil Corporation LTDDocument1 pageIndian Oil Corporation LTDAjay HariharanNo ratings yet