You might also like

- Chapter 10 Discounted DividendDocument5 pagesChapter 10 Discounted Dividendmahnoor javaidNo ratings yet

- How Brands Can Enter The MetaverseDocument7 pagesHow Brands Can Enter The MetaverseAmna NasserNo ratings yet

- Answers to Selected Problems in Multivariable Calculus with Linear Algebra and SeriesFrom EverandAnswers to Selected Problems in Multivariable Calculus with Linear Algebra and SeriesRating: 1.5 out of 5 stars1.5/5 (2)

- Ldis and RapidsDocument28 pagesLdis and RapidsRheii EstandarteNo ratings yet

- Chapter 4 International Trade TheoryDocument40 pagesChapter 4 International Trade TheoryAtiqul IslamNo ratings yet

- Customer Service Case StudiesDocument4 pagesCustomer Service Case Studiessameer maddubaigari80% (5)

- Kunci JWB Soal B 2015 PDFDocument29 pagesKunci JWB Soal B 2015 PDFAnisaa Okta100% (5)

- Answer Key Chap 4Document9 pagesAnswer Key Chap 4itsaljaneNo ratings yet

- Interest Rate Answer by BrighamDocument15 pagesInterest Rate Answer by BrighamBrandon LumibaoNo ratings yet

- s1054343 TMA1Document10 pagess1054343 TMA1Jason LamNo ratings yet

- Solutions - Chapter 11Document3 pagesSolutions - Chapter 11sajedulNo ratings yet

- Tannous1e SSM Chapter 2Document12 pagesTannous1e SSM Chapter 2Shikha NandNo ratings yet

- Module 4 Activity 1Document5 pagesModule 4 Activity 1Arnelli GregorioNo ratings yet

- Examinations: Subject 102 - Financial MathematicsDocument11 pagesExaminations: Subject 102 - Financial MathematicsClerry SamuelNo ratings yet

- Final Corpo 2018 SolutionDocument11 pagesFinal Corpo 2018 Solutionadrien.graffNo ratings yet

- Forward Rates Bond ReturnsDocument5 pagesForward Rates Bond ReturnsSaurav KumarNo ratings yet

- Session 6 SolutionsDocument36 pagesSession 6 SolutionsAnu AmruthNo ratings yet

- Team4 FmassignmentDocument10 pagesTeam4 FmassignmentruchirNo ratings yet

- Answer The Short Answer Questions in A Separate Word Document and Clearly Show All Your WorkDocument4 pagesAnswer The Short Answer Questions in A Separate Word Document and Clearly Show All Your WorkTalhaa MaqsoodNo ratings yet

- Solution For Numerical Review QuestionDocument85 pagesSolution For Numerical Review QuestionAparajith GuhaNo ratings yet

- K D K D K D K D V: Muqaddas ZubairDocument5 pagesK D K D K D K D V: Muqaddas ZubairMahlab RajpootNo ratings yet

- Clase 4 Ingenieria EconomicaDocument55 pagesClase 4 Ingenieria EconomicaGrupo de Estudios FincosmerNo ratings yet

- FM Textbook Solutions Chapter 8 Second EditionDocument11 pagesFM Textbook Solutions Chapter 8 Second EditionlibredescargaNo ratings yet

- CHAPTER 4: Practice Questions (Page 82)Document4 pagesCHAPTER 4: Practice Questions (Page 82)ALLtyNo ratings yet

- Assignment UploadDocument7 pagesAssignment UploadSiddarth BaligaNo ratings yet

- Week 6 Tutorial SolutionsDocument8 pagesWeek 6 Tutorial SolutionsManoaNo ratings yet

- Pascals Triangle and Binomial WsDocument3 pagesPascals Triangle and Binomial WsJiwanshi ShahNo ratings yet

- CH 01 Bond Pricing - Ready-To-BuildDocument19 pagesCH 01 Bond Pricing - Ready-To-BuildShruti SankarNo ratings yet

- Bab Iii ISI: I. PerhitunganDocument9 pagesBab Iii ISI: I. PerhitunganRaevansya Arya KanigaraNo ratings yet

- FIN 301 B Porter Larac 3-4 Key2Document4 pagesFIN 301 B Porter Larac 3-4 Key2Sunny RajesthNo ratings yet

- SFM Suggested Answers PDFDocument352 pagesSFM Suggested Answers PDFAindrila BeraNo ratings yet

- FIN 630.assignmentDocument2 pagesFIN 630.assignmentMuhammad ArbazNo ratings yet

- FIN 630.assignmentDocument2 pagesFIN 630.assignmentMuhammad ArbazNo ratings yet

- University of Tunis Tunis Business SchoolDocument2 pagesUniversity of Tunis Tunis Business Schoolcyrine chahbaniNo ratings yet

- PGP/24/097 Paras Mavani: Indian Institute of Management Kozhikode, Post Graduate Programme PGP 24 - Section BDocument10 pagesPGP/24/097 Paras Mavani: Indian Institute of Management Kozhikode, Post Graduate Programme PGP 24 - Section BParas Mavani100% (1)

- F.M Rev 2019Document17 pagesF.M Rev 2019AA BB MMNo ratings yet

- Assignment SolutionDocument2 pagesAssignment SolutionMuhammad ArbazNo ratings yet

- QuasilikelihoodDocument14 pagesQuasilikelihoodK6 LyonNo ratings yet

- Compound Interest:: Log A Log P + Tlog (1+ R)Document3 pagesCompound Interest:: Log A Log P + Tlog (1+ R)Aachal SinghNo ratings yet

- How To Calculate Present Values: Discounted Cash Flow Analysis (Time Value of Money)Document16 pagesHow To Calculate Present Values: Discounted Cash Flow Analysis (Time Value of Money)cypriancourageNo ratings yet

- BA 2802 - Principles of Finance Solutions To Problems For Recitation #5Document7 pagesBA 2802 - Principles of Finance Solutions To Problems For Recitation #5Eda Nur EvginNo ratings yet

- Actuarial Society of India: ExaminationsDocument17 pagesActuarial Society of India: ExaminationsSonam SikkaNo ratings yet

- Seminar 2Document5 pagesSeminar 2EnnyNo ratings yet

- Investment AssinmentDocument8 pagesInvestment AssinmentKaleab TadesseNo ratings yet

- MidlandDocument1 pageMidlandcarlos.deoliveiraNo ratings yet

- Study Material - Most Imp Formulas - SI and CI Lyst4154Document7 pagesStudy Material - Most Imp Formulas - SI and CI Lyst4154Fight 4 FitnessNo ratings yet

- Example 3.1. Finding The Price and Yield To Maturity of A Coupon Bond Using Spot RatesDocument6 pagesExample 3.1. Finding The Price and Yield To Maturity of A Coupon Bond Using Spot RatesSalma ElNo ratings yet

- Time Value of MoneyDocument4 pagesTime Value of Moneyermirakastrati2004No ratings yet

- Financial Management FM Final PaperDocument13 pagesFinancial Management FM Final PaperSaqib AliNo ratings yet

- Sec 5.1: Mathematics of Finance Formulas:: Interest Is Compounded K Times A Year.: Interest Is Compounded ContinuouslyDocument5 pagesSec 5.1: Mathematics of Finance Formulas:: Interest Is Compounded K Times A Year.: Interest Is Compounded ContinuouslyAANo ratings yet

- Institute of Actuaries of India: November 2010 ExaminationsDocument9 pagesInstitute of Actuaries of India: November 2010 ExaminationsdasNo ratings yet

- Questions Exercises 2023Document10 pagesQuestions Exercises 2023Yến Nhi VũNo ratings yet

- Solution For Exercise #2Document5 pagesSolution For Exercise #2Lorman MaylasNo ratings yet

- BUS103 AssignmentDocument6 pagesBUS103 AssignmentRohit KarmakarNo ratings yet

- Financial Mathematics For Actuaries: Bond Management Learning ObjectivesDocument63 pagesFinancial Mathematics For Actuaries: Bond Management Learning ObjectivesRehabUddinNo ratings yet

- MAT ReportDocument25 pagesMAT ReportZunaeid Mahmud LamNo ratings yet

- Ct1 Iai 0509 Sol FinalDocument12 pagesCt1 Iai 0509 Sol FinalJakub Wojciech WisniewskiNo ratings yet

- Labs TP3y06Document48 pagesLabs TP3y06api-3856799No ratings yet

- Interest Rate RiskDocument25 pagesInterest Rate Riskmailinh1991No ratings yet

- Chapter 9: Capital Market Theory: An Overview: You Earned $500 in Capital GainsDocument14 pagesChapter 9: Capital Market Theory: An Overview: You Earned $500 in Capital GainsratikdayalNo ratings yet

- Lecture 6 TQ-SolutionDocument2 pagesLecture 6 TQ-SolutionHiền nguyễn thuNo ratings yet

- Tutorial 2 SolutionsDocument6 pagesTutorial 2 SolutionsFaryalNo ratings yet

- Fixed Income Solution ch3Document22 pagesFixed Income Solution ch3Pham Minh DucNo ratings yet

- Time Value Review Solutions TypedDocument1 pageTime Value Review Solutions TypedJavan OdephNo ratings yet

- Arslan Mubarak-18u00073 528 7449 144625Document1 pageArslan Mubarak-18u00073 528 7449 144625Amna NasserNo ratings yet

- Tropicana's Packaging Redesign FailureDocument8 pagesTropicana's Packaging Redesign FailureAmna NasserNo ratings yet

- Indus Valley CivilisationDocument4 pagesIndus Valley CivilisationAmna NasserNo ratings yet

- Microfinance Challenges and Opportunities in PakistanDocument10 pagesMicrofinance Challenges and Opportunities in PakistanAmna NasserNo ratings yet

- Iman Khurram Khan-18u00231 528 7449 383511Document2 pagesIman Khurram Khan-18u00231 528 7449 383511Amna NasserNo ratings yet

- "A Marketing Plan On Foster Protein Shake": ThesisDocument23 pages"A Marketing Plan On Foster Protein Shake": ThesisAmna NasserNo ratings yet

- When Sarojini Naidu Called Mohammad Ali JinnahDocument2 pagesWhen Sarojini Naidu Called Mohammad Ali JinnahAmna NasserNo ratings yet

- Starbucks CaseDocument1 pageStarbucks CaseAmna NasserNo ratings yet

- FMII Review of FM I Assignment 1 SolutionDocument2 pagesFMII Review of FM I Assignment 1 SolutionAmna NasserNo ratings yet

- Pakistan Studies Assignment 6Document1 pagePakistan Studies Assignment 6Amna NasserNo ratings yet

- Project Guidelines-Mahvesh Mahmud-Operations ManagementDocument7 pagesProject Guidelines-Mahvesh Mahmud-Operations Managementsarakhan0622No ratings yet

- Ahore Chool OF Conomics: Pakistan Studies (SSC 327)Document14 pagesAhore Chool OF Conomics: Pakistan Studies (SSC 327)Amna NasserNo ratings yet

- SOCIOLOGYDocument2 pagesSOCIOLOGYAmna NasserNo ratings yet

- Taxation Assignment 4Document2 pagesTaxation Assignment 4Amna NasserNo ratings yet

- FMII Review of FM I Assignment 1 SolutionDocument2 pagesFMII Review of FM I Assignment 1 SolutionAmna NasserNo ratings yet

- BCG Matrix Analysis UnileverDocument2 pagesBCG Matrix Analysis UnileverAmna NasserNo ratings yet

- BCG Matrix Analysis UnileverDocument2 pagesBCG Matrix Analysis UnileverAmna NasserNo ratings yet

- Lecture 18CAs20Document40 pagesLecture 18CAs20mzNo ratings yet

- FM 1 Assignment 6 Solution - 2019Document3 pagesFM 1 Assignment 6 Solution - 2019Amna NasserNo ratings yet

- Receivables Sales/365: Lahore School of Economics Financial Management II Working Capital Management - 3 Assignment 18Document3 pagesReceivables Sales/365: Lahore School of Economics Financial Management II Working Capital Management - 3 Assignment 18SinpaoNo ratings yet

- Chap 10 IM Common Stock ValuationDocument84 pagesChap 10 IM Common Stock ValuationAmna NasserNo ratings yet

- Advertising - Assignment 1: Abdul Ahad Ali Humaira Amir Mahnoor Riaz Syeda Leeva Abdullah Talha Omer ButtDocument9 pagesAdvertising - Assignment 1: Abdul Ahad Ali Humaira Amir Mahnoor Riaz Syeda Leeva Abdullah Talha Omer ButtAmna NasserNo ratings yet

- SOCIOLOGYDocument2 pagesSOCIOLOGYAmna NasserNo ratings yet

- Supply Chain Assignment 1Document3 pagesSupply Chain Assignment 1Amna NasserNo ratings yet

- Communicating in Today's Workplace: Business Communication: Process and Product, 6eDocument19 pagesCommunicating in Today's Workplace: Business Communication: Process and Product, 6eAmna NasserNo ratings yet

- The Impact of Government Policy and Regulation On BankingDocument15 pagesThe Impact of Government Policy and Regulation On BankingAmna Nasser100% (1)

- The Impact of Government Policy and Regulation On BankingDocument15 pagesThe Impact of Government Policy and Regulation On BankingAmna Nasser100% (1)

- Mistakes Exporters Make: Export Marketing Spring 2021Document10 pagesMistakes Exporters Make: Export Marketing Spring 2021Amna NasserNo ratings yet

- Foreign Exchange Rates (FOREX)Document2 pagesForeign Exchange Rates (FOREX)LSTNo ratings yet

- HTM 220 Assignment #4Document2 pagesHTM 220 Assignment #4Annie ChoiNo ratings yet

- UiTM SHAH ALAM PUBLIC TRANSPORT SERVICE (LATEST)Document4 pagesUiTM SHAH ALAM PUBLIC TRANSPORT SERVICE (LATEST)Khairul AnazNo ratings yet

- Arce - Chan Accounting FirmDocument38 pagesArce - Chan Accounting FirmshaneNo ratings yet

- PS Review Chapter 4Document8 pagesPS Review Chapter 4Thai Quoc Toan (K15 HCM)No ratings yet

- Miles Mathis Guest Writer - Fridges (And Other Musings)Document10 pagesMiles Mathis Guest Writer - Fridges (And Other Musings)Evgyrt NesralNo ratings yet

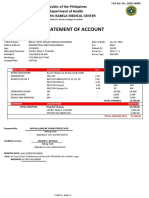

- Statement of Account: Republic of The Philippines Department of Health Southern Isabela Medical CenterDocument1 pageStatement of Account: Republic of The Philippines Department of Health Southern Isabela Medical CenterNHUJBETH INTERNET CAFENo ratings yet

- Rs. 113.7 Rs.38739.92 Rs.38821.43: Account Statement ForDocument3 pagesRs. 113.7 Rs.38739.92 Rs.38821.43: Account Statement Forirfan shamaNo ratings yet

- Bahrain ChemicalDocument4 pagesBahrain Chemicallokesh LokiNo ratings yet

- Census and Statistics Department Hong Kong Special Administrative RegionDocument1 pageCensus and Statistics Department Hong Kong Special Administrative Regionka yee lauNo ratings yet

- Ies TomDocument42 pagesIes TomLidiaCojocaruNo ratings yet

- Module 4 - DepreciationDocument70 pagesModule 4 - DepreciationGaurav ShekharNo ratings yet

- CTM Machine-Global QuotationDocument5 pagesCTM Machine-Global QuotationGanesh Kumar TulabandulaNo ratings yet

- Plan de Formación para El Cuidado en Tiempos de Covid-19 (Agosto 2020) v1.0 (1-150)Document80 pagesPlan de Formación para El Cuidado en Tiempos de Covid-19 (Agosto 2020) v1.0 (1-150)leidy marcela mercado ibanezNo ratings yet

- Line No 1Document59 pagesLine No 1manoharahrNo ratings yet

- Brosur ARIN PARTITIONDocument12 pagesBrosur ARIN PARTITIONMomo mwsNo ratings yet

- Product Inventory - XLSX - May 2022Document1 pageProduct Inventory - XLSX - May 2022CRISTINE JOY LAUZNo ratings yet

- Furniture and Wood Pakistan ImporterDocument10 pagesFurniture and Wood Pakistan ImporterSheroz AhmedNo ratings yet

- Economics 2142 Time Series Analysis SyllabusDocument14 pagesEconomics 2142 Time Series Analysis SyllabusGabriel RoblesNo ratings yet

- Summary For The Preparation of Bank Reconciliation StatementDocument5 pagesSummary For The Preparation of Bank Reconciliation StatementGhalib HussainNo ratings yet

- Date Received From Branch Reference Amount: Total Collections 371,905.17 Total Available Cash 527,546.92Document1 pageDate Received From Branch Reference Amount: Total Collections 371,905.17 Total Available Cash 527,546.92Merliza JusayanNo ratings yet

- BanKO Partner Outlet LocatorDocument344 pagesBanKO Partner Outlet LocatorBPI Globe BanKONo ratings yet

- Vietnam May 23Document8 pagesVietnam May 23ImpExp TradeNo ratings yet

- 8085 22555 1 PBDocument6 pages8085 22555 1 PBAlief RachmanNo ratings yet

- 2 TsgraphicsDocument107 pages2 TsgraphicsjuanivazquezNo ratings yet

- National Institute of Plant Health ManagementDocument5 pagesNational Institute of Plant Health ManagementVinodkumar NaikNo ratings yet