You might also like

- Dokumen Persediaan TapakDocument4 pagesDokumen Persediaan TapakFathoni UsmanNo ratings yet

- Nota Kepada AkaunDocument12 pagesNota Kepada AkaunAdleena SyafiqaNo ratings yet

- Bab 7 FiqhDocument27 pagesBab 7 FiqhsyaziqahkittyNo ratings yet

- Sukuk - Assignment Paper PDFDocument14 pagesSukuk - Assignment Paper PDFHud SabriNo ratings yet

- Panduan Mengisi Borang Ckht1aDocument5 pagesPanduan Mengisi Borang Ckht1aAlyssia LohNo ratings yet

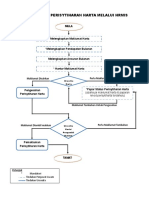

- Carta Aliran HARTADocument1 pageCarta Aliran HARTAGollip PasokNo ratings yet

- Cukai Keuntungan Harta TanahDocument26 pagesCukai Keuntungan Harta TanahDarling Tuna100% (3)

- Asas HartanahDocument2 pagesAsas HartanahAmrun100% (1)

- Strata 2 UDocument3 pagesStrata 2 UMohd FaizNo ratings yet

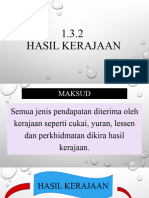

- 5 - 1.3.2 - Hasil KerajaanDocument18 pages5 - 1.3.2 - Hasil KerajaanGood KIDSNo ratings yet

- Pendapatan DaerahDocument16 pagesPendapatan DaerahAyme Stasia ClorindaNo ratings yet

- Teach in Bil 7 2019Document82 pagesTeach in Bil 7 2019MUHD ROSHASANUL ISYRAF BIN ABD WAHIDNo ratings yet

- 05.pajak Dan Retribusi DaerahDocument22 pages05.pajak Dan Retribusi DaerahTaufikdayat08 0303No ratings yet

- 2.0 Pengenalan Perakaunan AkruanDocument32 pages2.0 Pengenalan Perakaunan Akruansme_78No ratings yet

- 323-Panduan Ringkas-Tempat Letak KeretaDocument7 pages323-Panduan Ringkas-Tempat Letak KeretaGangaaNo ratings yet

- CKHT 1a 2021Document9 pagesCKHT 1a 2021shazuarni ahmadNo ratings yet

- Jawapan Tutorial Syarikat AccDocument8 pagesJawapan Tutorial Syarikat AccSiti NurfatehahNo ratings yet

- Ainul PresentDocument29 pagesAinul PresentDanial AfiqNo ratings yet

- Pengurusan SrataDocument17 pagesPengurusan SrataHafizzuddin AnuarNo ratings yet

- Modul 2Document3 pagesModul 2NURUL SHAHRINI KASIANNo ratings yet

- Bersama Membangun Negara: Pengenalan Pelupusan Yang Tidak Dikenakan CKHTDocument1 pageBersama Membangun Negara: Pengenalan Pelupusan Yang Tidak Dikenakan CKHTcakur079026No ratings yet

- Modul 8 - Pelarasan Pada Tarikh Imbangan Dan Penyediaan Penyata Kewangan Milikan TunggalDocument11 pagesModul 8 - Pelarasan Pada Tarikh Imbangan Dan Penyediaan Penyata Kewangan Milikan Tunggalnr dawesyaNo ratings yet

- Brosur Pengambilan Tanah BMDocument2 pagesBrosur Pengambilan Tanah BMunclebendittoNo ratings yet

- Bab 6:analisis Penyata KewanganDocument14 pagesBab 6:analisis Penyata KewanganAmira NatasyaNo ratings yet

- Garis Panduan CKHT 20230106Document83 pagesGaris Panduan CKHT 20230106En ShahNo ratings yet

- Kuliah Cukai Keuntungan Hartanah-UpdatedDocument30 pagesKuliah Cukai Keuntungan Hartanah-UpdatedAzyan NajNo ratings yet

- Perolehan Ict & Ketidak Patuhan & DaruratDocument17 pagesPerolehan Ict & Ketidak Patuhan & DaruratfazliNo ratings yet

- Kaveat Dan KebaikanDocument9 pagesKaveat Dan KebaikanSiti Noor MardianaNo ratings yet

- Slide Bicara Santai Siri 2 V2Document24 pagesSlide Bicara Santai Siri 2 V2Farah Wahida IbrahimNo ratings yet

- Tajuk 2 Klasifikasi Akaun Alephb Dan Akaun KontraDocument50 pagesTajuk 2 Klasifikasi Akaun Alephb Dan Akaun KontraSyarafina AbdullahNo ratings yet

- Pengenalan Pengurusan StrataDocument31 pagesPengenalan Pengurusan StrataAhmad FarhanNo ratings yet

- Flowchart Aktiva TetapDocument13 pagesFlowchart Aktiva TetapGaluh YusnindarNo ratings yet

- Dasar Pemilikan Hartanah Oleh Warganegara Asing Untuk Memiliki Hartanah Di Negeri MelakaDocument5 pagesDasar Pemilikan Hartanah Oleh Warganegara Asing Untuk Memiliki Hartanah Di Negeri MelakaKamarul Ramdani ZulkifliNo ratings yet

- Pengurusan HasilDocument60 pagesPengurusan Hasiluhisyam sriibNo ratings yet

- RPM Math Tahun 5Document3 pagesRPM Math Tahun 5watashi waNo ratings yet

- Matrik Ev RPD Kab Hulu Sungai Tengah TTG PBB P2Document11 pagesMatrik Ev RPD Kab Hulu Sungai Tengah TTG PBB P2Amieng WijayaNo ratings yet

- Nota ACC S1Document18 pagesNota ACC S1Safierah QistinaNo ratings yet

- Penyata KewanganDocument12 pagesPenyata KewanganMay LeeNo ratings yet

- Strata Handbook 2.0Document27 pagesStrata Handbook 2.0Larry B100% (1)

- Eko-Rainforest Perisytiharan Jualan (20201222)Document17 pagesEko-Rainforest Perisytiharan Jualan (20201222)moustaphaNo ratings yet

- Bab 12 - Akuntansi Transaksi IjarahDocument58 pagesBab 12 - Akuntansi Transaksi IjarahSuazhari IbrahimNo ratings yet

- 1.31 - BM - MG - Water Supply Services AgreementDocument2 pages1.31 - BM - MG - Water Supply Services AgreementganmalNo ratings yet

- LatihanDocument14 pagesLatihanImmea IshNo ratings yet

- Kewpa 14Document3 pagesKewpa 14Sii leh teingNo ratings yet

- Bab 3 Matematik Pengguna: Insurans: 3.1 Risiko Dan Perlindungan InsuransDocument18 pagesBab 3 Matematik Pengguna: Insurans: 3.1 Risiko Dan Perlindungan InsuransNUR RAIHAN BINTI ABDUL RAHIM MoeNo ratings yet

- Nota Matematik Tingkatan 5 BAB 4-MATEMATIK PENGGUNA PERCUKAIANDocument3 pagesNota Matematik Tingkatan 5 BAB 4-MATEMATIK PENGGUNA PERCUKAIANCROSS GENE MALAYSIA FBNo ratings yet

- Perbezaan Prosedur Harta Pusaka KecilDocument3 pagesPerbezaan Prosedur Harta Pusaka Kecilnurulhanan0910No ratings yet

- Basis Data JojDocument18 pagesBasis Data JojPapua ChanelNo ratings yet

- CBCRDocument36 pagesCBCRpsikomagicNo ratings yet

- CMPFi PDS BM BR2.65 V3.9Document5 pagesCMPFi PDS BM BR2.65 V3.9MOHAMMAD ZURAIRI IBRAHIMANo ratings yet

- Aspek Perbezaan Antara Organisasi PerniagaanDocument3 pagesAspek Perbezaan Antara Organisasi Perniagaanshikeen_adlyNo ratings yet

- 1.1 Aliran Pusingan Pendapatan Negara-RASYIDDocument9 pages1.1 Aliran Pusingan Pendapatan Negara-RASYIDazreen fairuzNo ratings yet

- Jawapan Modul02Document5 pagesJawapan Modul02Nur AqilahNo ratings yet

- Slaid Percukaian KoperasiDocument55 pagesSlaid Percukaian KoperasiNazrilMizarNo ratings yet

- Taklimat Kajian IklanDocument21 pagesTaklimat Kajian IklanNurul HidayahNo ratings yet

- Taklimat PK 1 Punca Kuasa, Prinsip Dan Dasar Perolehan KerajaanDocument41 pagesTaklimat PK 1 Punca Kuasa, Prinsip Dan Dasar Perolehan KerajaanENCIK MOHD YUSLIZAN BIN OTHMAN (POLIMELAKA)No ratings yet

- KHIYARDocument10 pagesKHIYARAdriana AzmanNo ratings yet

- 11.ekonomi GIGDocument26 pages11.ekonomi GIGAhmad YusriNo ratings yet

- 10.ekonomi BayanganDocument8 pages10.ekonomi BayanganAhmad YusriNo ratings yet

- 9.ekonomi DigitalDocument8 pages9.ekonomi DigitalAhmad YusriNo ratings yet

- 3.majikan Dan PekerjaDocument18 pages3.majikan Dan PekerjaAhmad YusriNo ratings yet